Setting the pace to drive 5G consumer business growth

- English

- 繁體中文

Our new ConsumerLab report, the first industry study of its kind, looks at 73 service providers in 22 markets across the world, analyzing their market performance and consumer perception to form a 5G Maturity Index. Using the data collected, we identified four stages of 5G maturity, from 5G Explorers to 5G Pacesetters – those leading the charge in both performance and innovation – and highlight the six strategies they have used to get to this position.

Measuring 5G progress and maturity

Key findings

Methodology

The 5G Maturity Index tracks each service provider’s progress in their 5G consumer business by assessing 105 criteria across 16 categories. The consumer perception data forms 50 percent of the index results, while the remaining 50 percent is based on service providers’ publicly reported information around 5G progress. Consumers in 22 markets were asked to provide importance ratings for different criteria, as well as satisfaction ratings for service providers in their local market. The four stages of 5G maturity have therefore been defined based on each of the 73 service providers’ total index scores out of a theoretical maximum of 100. The scores for the top performers, the 5G Pacesetters, range from 49 to 62 points, while the lowest scorers, the 5G Explorers, range from 21 to 29 points.

Figure 1: Methodology and structure of the 5G Maturity Index

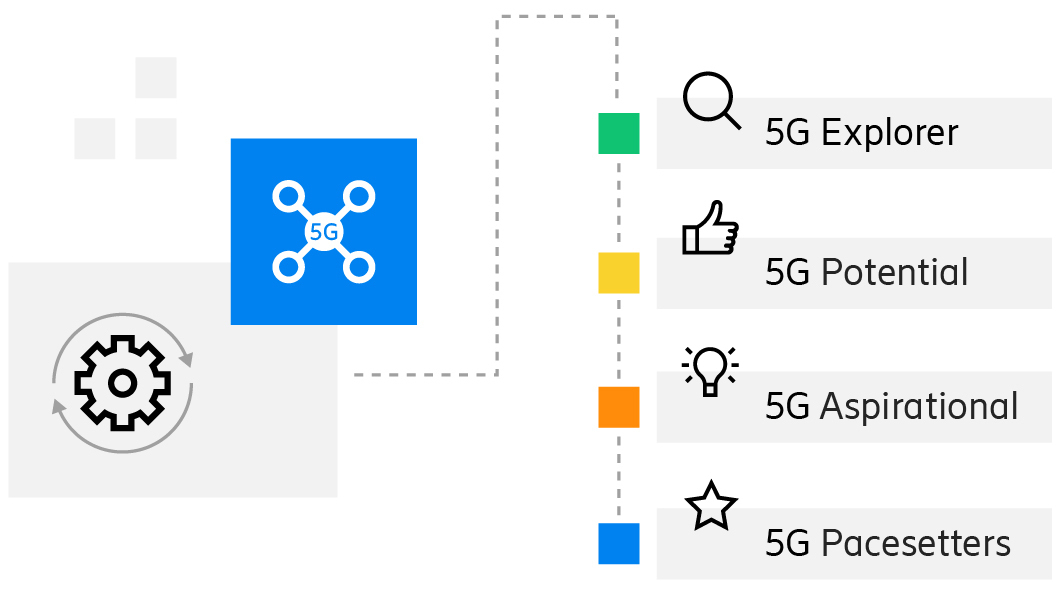

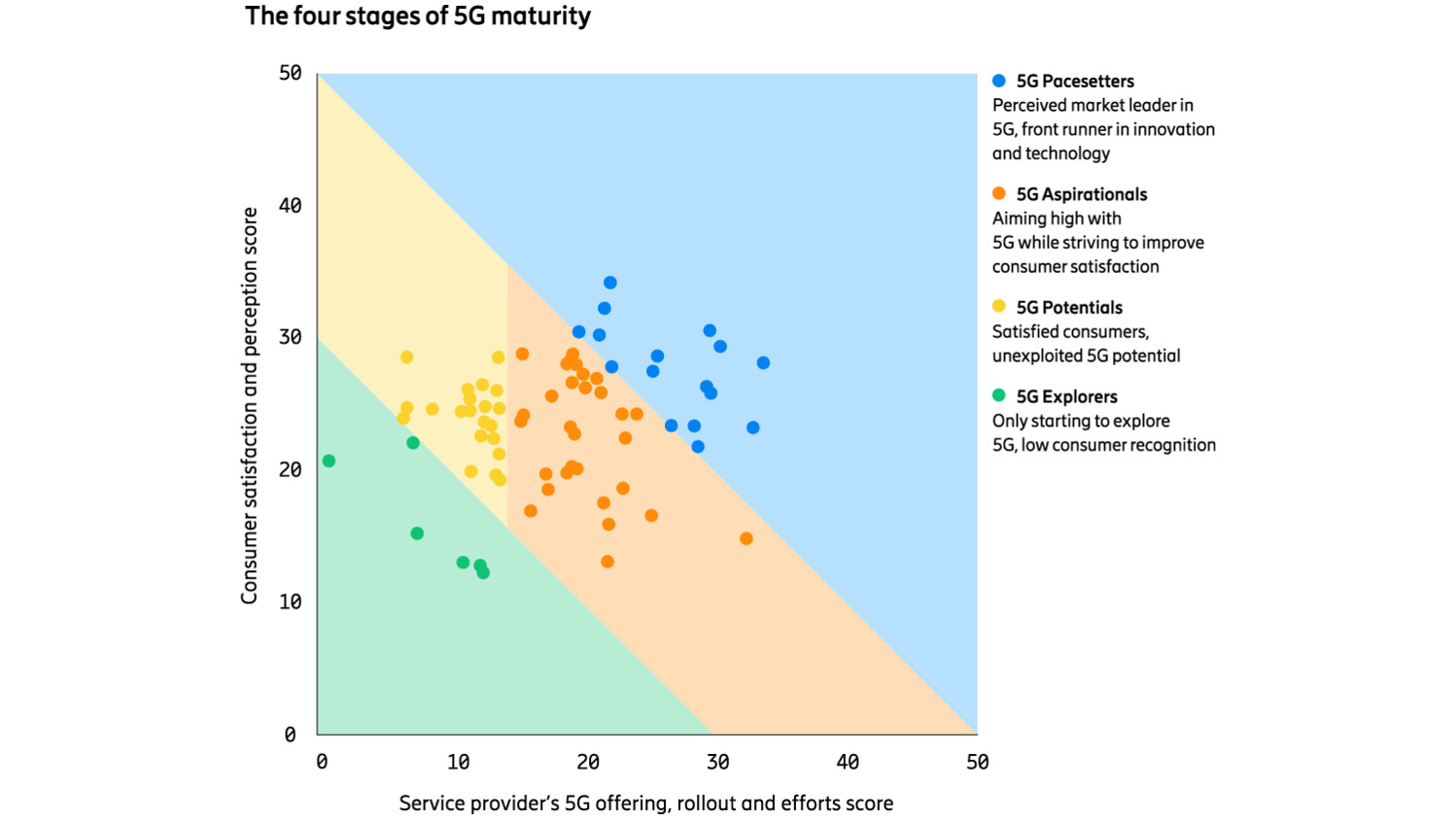

The four stages of 5G maturity

5G Explorers

These are often the market price challengers, trailing behind other service providers in all areas of consumer satisfaction and 5G investment. They have only recently started to explore the 5G market, often with limited spectrum holdings or allocations.

5G Potentials

These are often rewarded for value for money by their local markets’ consumers. However, they have so far done little to innovate, particularly in accelerating 5G network coverage rollout or introducing new 5G services.

5G Aspirationals

These are usually the market challengers that follow closely behind the 5G Pacesetters in 5G coverage, services and offerings. However, they often miss out on high consumer satisfaction and score lower on consumer perception of 5G market leadership and recommendation of their brand.

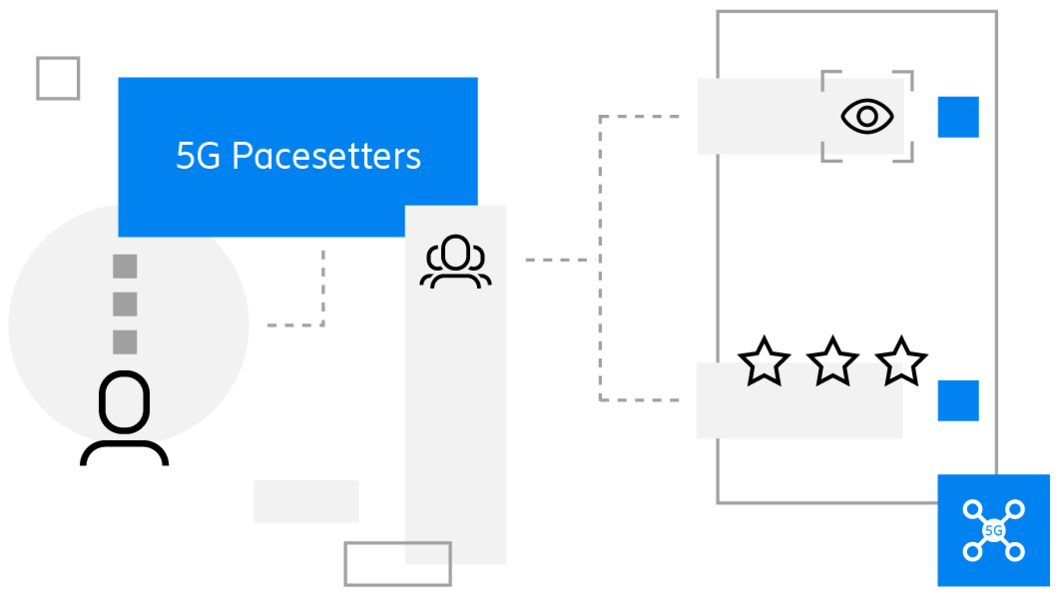

5G Pacesetters

These are the perceived 5G market leaders. They outpace their market competitors in 5G network coverage and speed and have invested most into new immersive 5G services and content partnerships to drive differentiation and eventually accelerate the uptake, usage and monetization of 5G.

Figure 2: The four stages of 5G maturity

Winning in the eyes of consumers

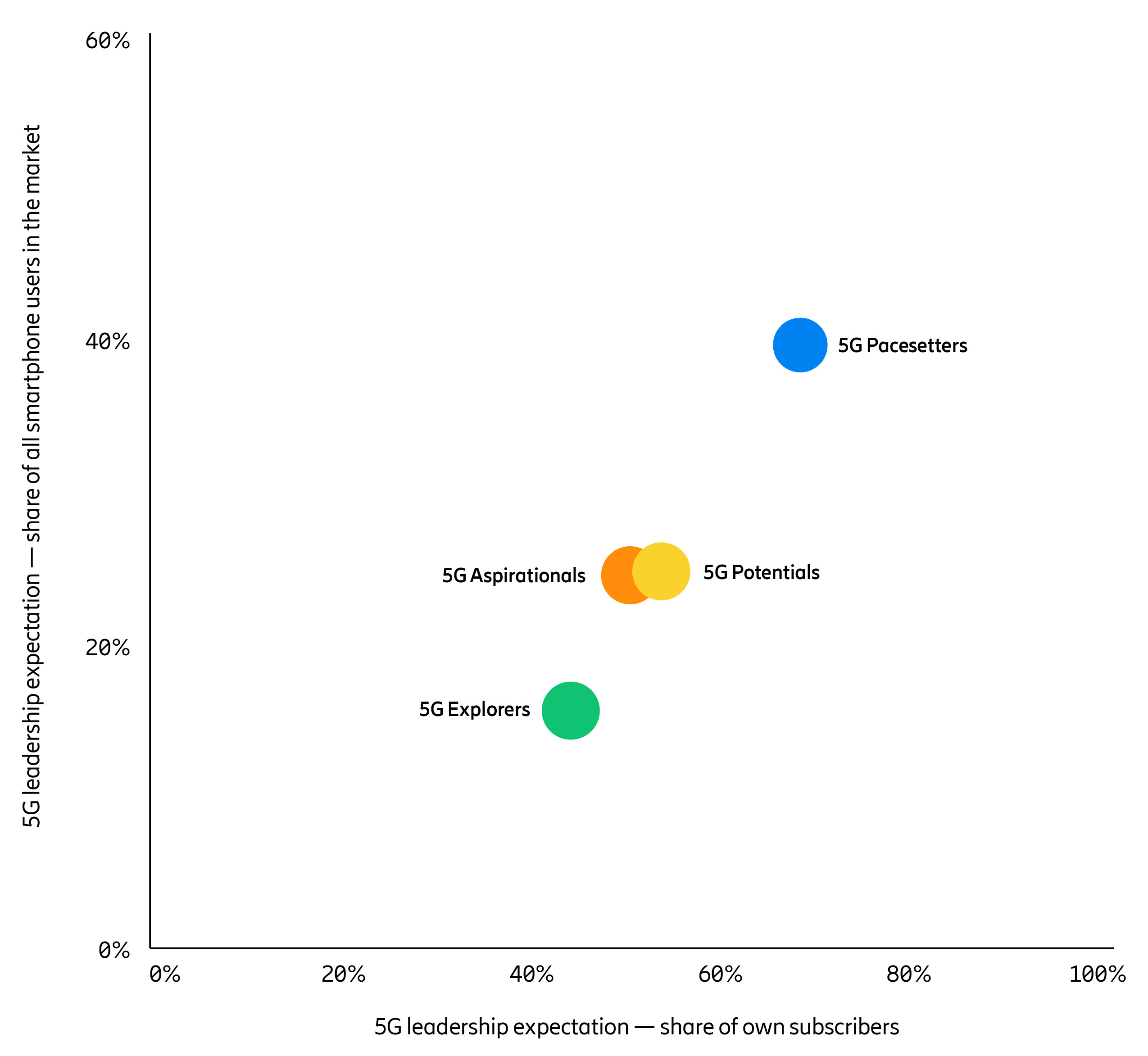

The customers of 5G Pacesetters rate them higher than other service providers in all aspects, including network coverage and quality, brand visibility, sales channel presence, innovative services, devices, customer service quality and tariff plans. The only exception is price and affordability.

Besides scoring higher than the competition in most criteria, 5G Pacesetters are also expected to lead their local markets in 5G. A clear majority of consumers (including 70 percent of their own customers) expect Pacesetters to dominate the 5G race. Only 17 percent of 5G Pacesetter customers think otherwise, while the remaining 13 percent are not aware. In contrast, 51 percent of non-Pacesetter customers don’t see their service provider as the leader in 5G.

Figure 4: 5G Pacesetters are perceived as leaders in 5G

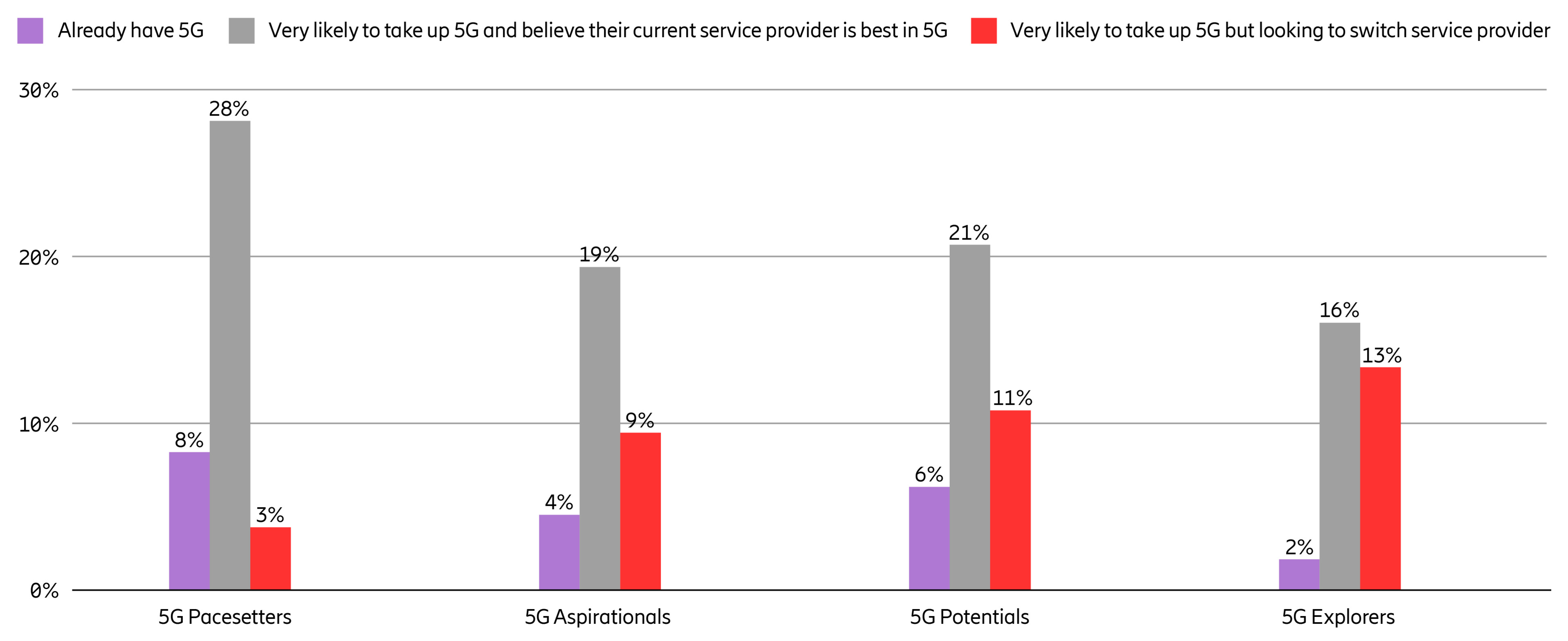

5G Pacesetters drive consumer demand for 5G by not only improving the perception of network availability and coverage among consumers, but also via effective marketing, and launching innovative services. 5G Pacesetters have around 50 percent more subscribers looking to upgrade to 5G compared to all other service providers, and a closer look at the data shows that subscribers of 5G Pacesetters are likely to stay with their current provider rather than making the switch.

Figure 5: Consumer intention to take up and switch providers for 5G

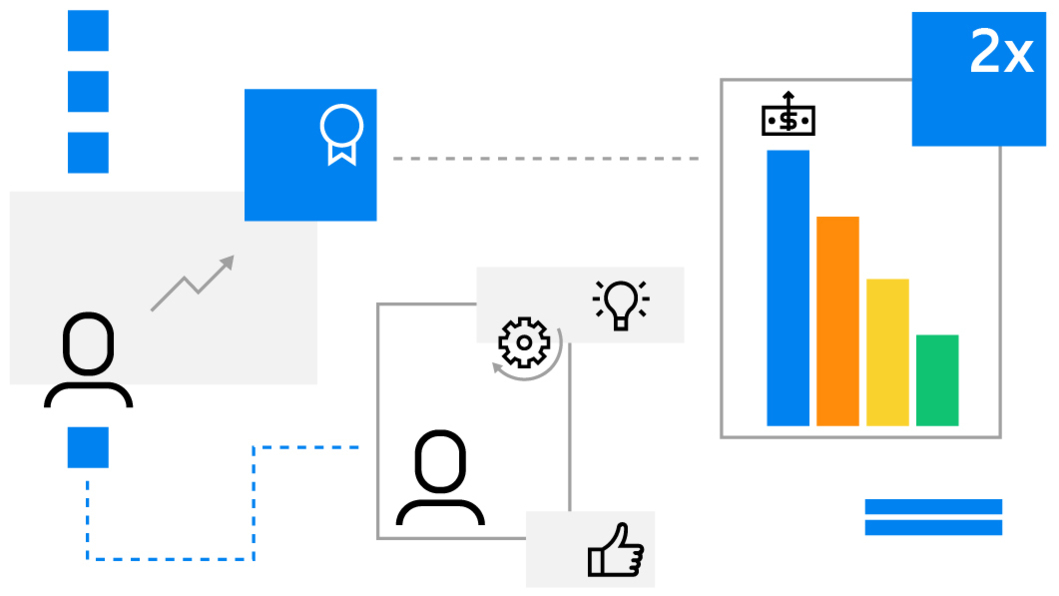

Growing 5G consumer revenues

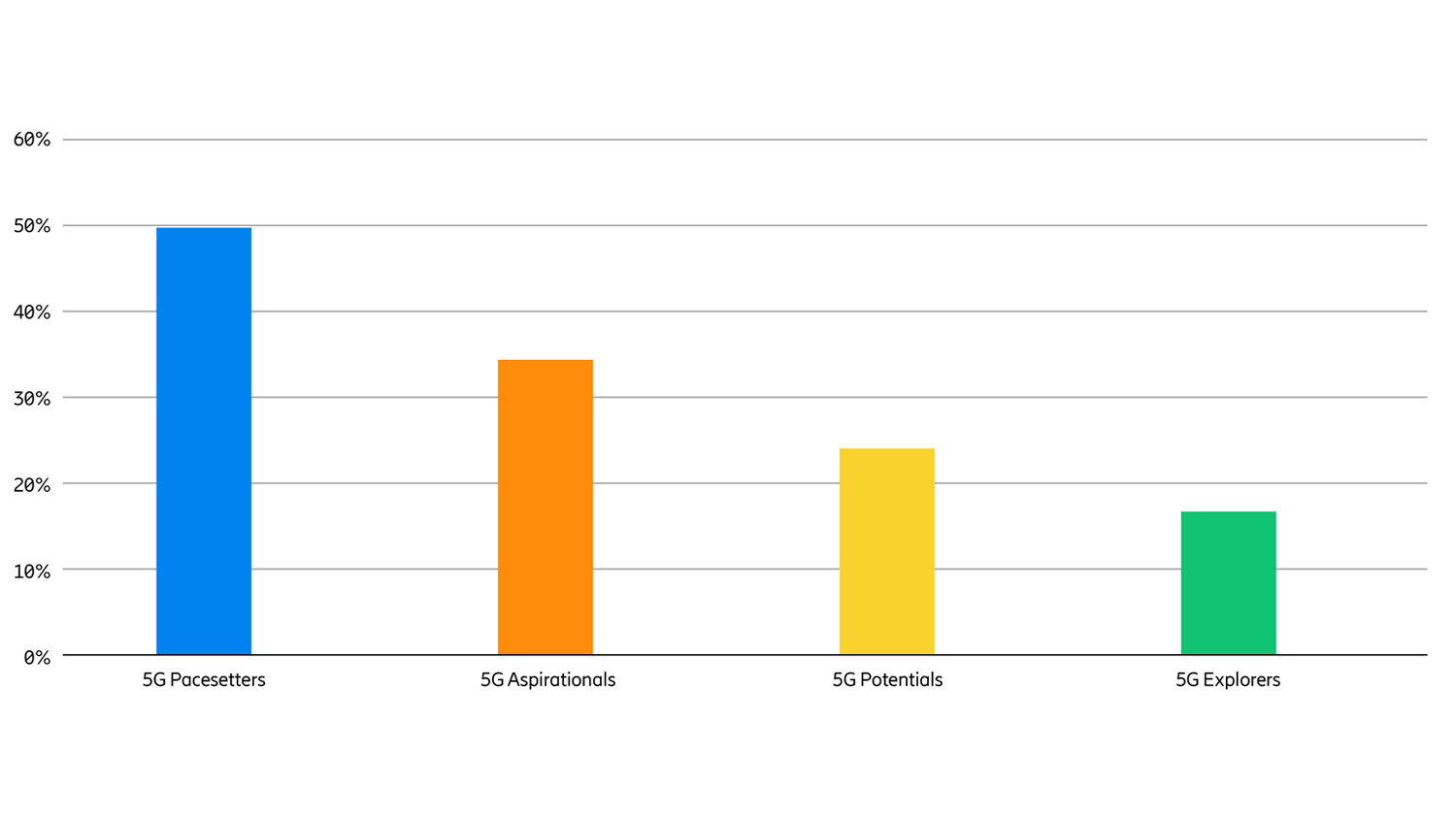

Our analysis uncovers how the financial performance and business strategies vary depending on the maturity of the service provider. It should be noted that not all service providers charge a price premium for 5G and yet, despite the impact of COVID-19, 50 percent of 5G Pacesetters grew their ARPU by at least 1 percent between Q1 2020 and Q1 2021.

In contrast, only 34 percent of 5G Aspirationals, 24 percent of 5G Potentials and just 17 percent of 5G Explorers were able to witness a positive development in ARPU. While this is not the result of 5G alone, in the case of 5G Pacesetters, the ARPU uplift is largely attributable to the service providers’ success in migrating consumers to premium 5G plans.

Not only could a higher share of 5G Pacesetters grow their ARPU year-on-year, but some 53 percent grew their mobile service revenues by 1 percent or more during the same period, while 20 percent saw their revenues decline by at least 1 percent. During this period, some 5G Pacesetters were even able to grow mobile service revenues by 7–8 percent. In contrast, only 30 percent of other service provider segments saw a positive development in mobile services revenues, and about half experienced a decline.

Figure 6: 5G maturity stages and share of service providers with at least 1 percent growth in ARPU Q1 2020–Q1 2021

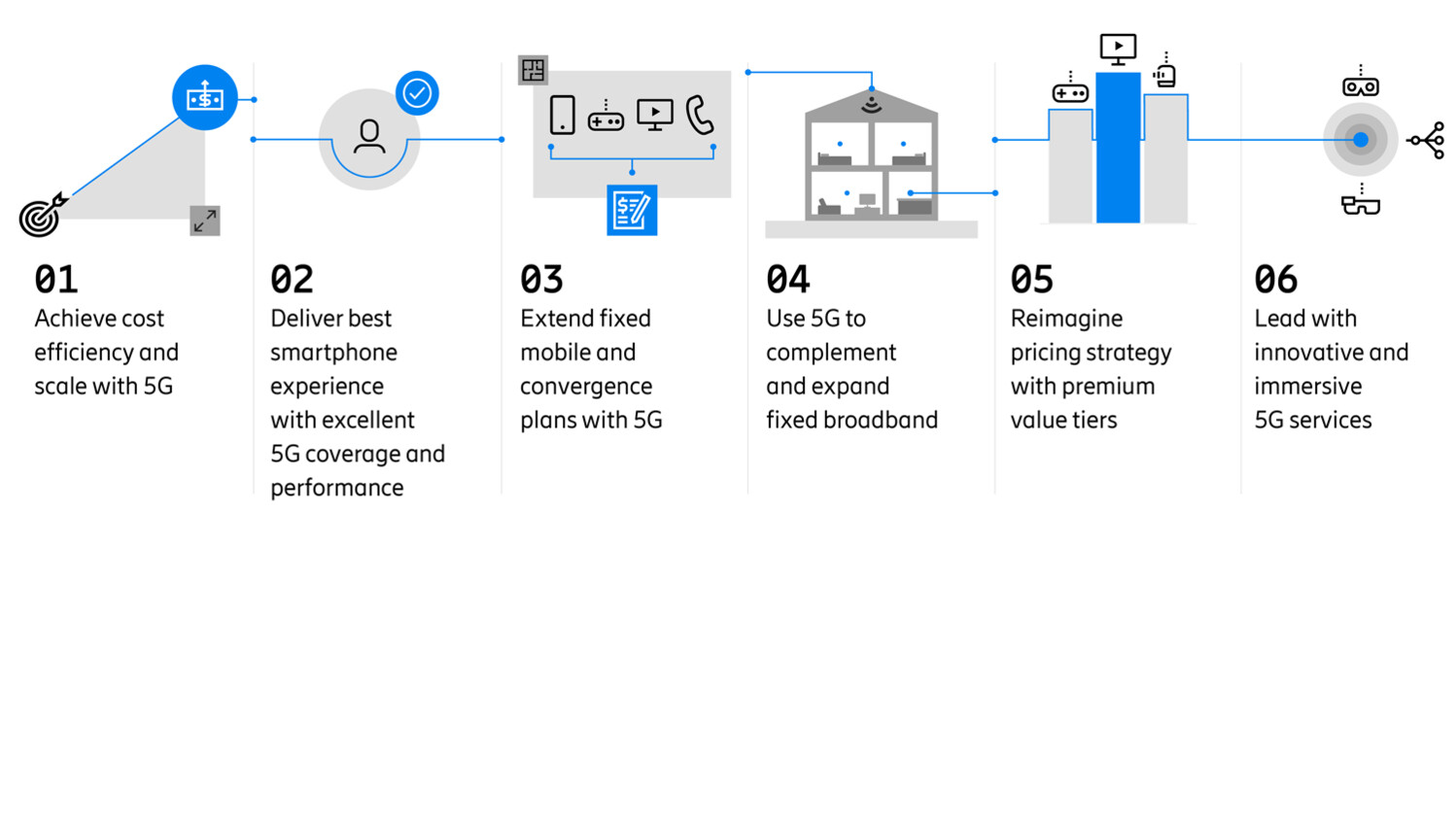

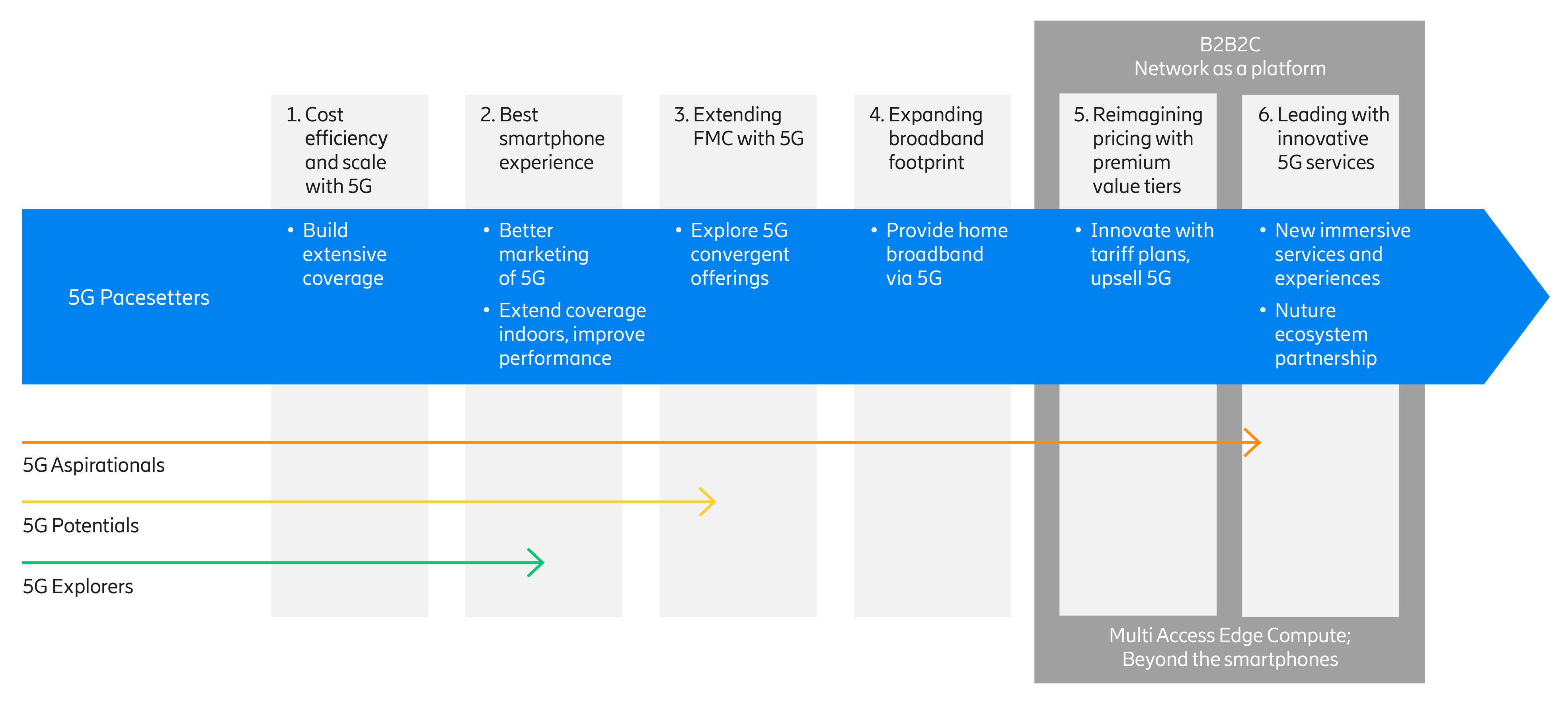

The six strategies 5G Pacesetters use to get ahead

The six strategies outline how 5G Pacesetters have been able to not only meet consumer expectations but also monetize 5G successfully. Particularly in markets with higher-than-average data usage, 5G Pacesetters and 5G Aspirationals deploy 5G coverage quickly and extensively to realize a long-term, more cost-efficient production engine for mobile data, with the possibility of supporting a significantly higher traffic demand now and in the future.

After ensuring cost-efficient operations, service providers deliver the best smartphone experience by using 5G to boost capacity and speed, particularly indoors and in key locations where the usage is high. The third strategic option identified in our study – extending Fixed Mobile Convergence (FMC) with 5G – is where service providers with fiber, TV and entertainment, and mobile assets, often bundle 5G mobile offerings into FMC plans for their household customers. Relying on the extensive 5G mobile coverage that complements their home broadband, these service providers’ household customers benefit from a seamless fiber-like experience in- and outside of the home. Service providers have also been using 5G to complement their fixed broadband footprint in areas where fiber isn’t available. They also use 5G to explore new revenue streams in the broadband market using 5G FWA to compete with incumbent broadband providers relying on DSL or cable.

The fifth strategy is about reimagining 5G pricing strategy with premium value tiers. In markets where tiered unlimited data volume plans have become a natural part of consumer offerings, service providers have been successful in upselling higher value 5G plans or price tiers to customers, based on either speed, quality of service, or content. An alternate way of monetizing 5G is by leading with innovative 5G services, in which service providers start to offer new immersive 5G services and event experiences for consumers to differentiate a 5G from a 4G experience.

Figure 8: Strategic options for the 5G consumer market and related paths to growth