At the end of the 1990s, the growth of GSM beat all previous world records. In 1998, the number of GSM subscribers totaled 100 million. At the end of the decade two years later, the figure was 465 million – more than the number of internet users, then estimated at 399 million. If other mobile telephony systems are included, the total number of mobile phone subscribers at the beginning of 2000 amounted to 760 million.

There was no stop to this stock-market hysteria in the New Year. On March 2, 2000, Dagens Industri reported: “The new economy has led to an explosion in trading on the Stockholm Stock Exchange. During the first two months of the year, turnover has risen by 107 percent to SEK 786 billion. Banks, stockbrokers and OM, the company that owns the exchange, are sitting on a goldmine.”

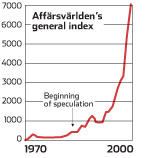

On Monday, March 6, the Stockholm General Index (Affärsvärldens Generalindex) closed at 6,961 points, another historic high. The total stock value was SEK 4,800 billion, twice as much as Sweden’s GDP. The most frequently traded stock was Ericsson’s, which at the time was considered to be worth SEK 1,800 billion.

3G LICENSES

This was the setting in which European countries were about to allocate licenses for the next generation of mobile telephone networks. EU politicians agreed that rapid expansion of 3G was vital for European development.

It was left to each individual country to decide which operators were to be allowed to build and run the networks. In the end, the licenses were allocated on two different principles: auctions or “beauty contests”.

Auctions took place in nine EU countries during 1999 and 2000. Bidders had to meet certain basic demands but then those offering the highest prices got the licenses. In this way the politicians counted on good revenues for the government finances.

And that is what they got. In all the operators paid just over 130 billion (which corresponded to about SEK 1,200 billion) for the licenses, which meant the right to build and run 3G networks. For comparison, Ford paid SEK 50 billion when it bought Volvo Cars, and the bridge between Sweden and Denmark cost SEK 20 billion.

Here too the Nordic countries took a different approach. Finland had already allocated four 3G licenses in March 1999 without imposing any coverage or timetable conditions on the operators. Sweden allocated four licenses and Norway three with stringent demands. Denmark waited until September 2001 and then auctioned four licenses with specifications that can be described as realistic.

The prevailing attitude was that the development of mobile telephony was to be based on social benefit, not viewed primarily as a source of revenue. There were advocates of the auction approach, which was rejected in Sweden with reference to the legal requirement that license fees were not allowed to be greater than the amount needed to cover the administrative costs of the supervisory agency.

TELIA GOT NOTHING

In Sweden, the decision of the Swedish Post and Telecom Agency (PTS), on December 16, 2000, to award the licenses to Europolitan (which later became Vodafone and then Telenor), Hi3G (later 3), Orange (which was acquired by France Telecom) and Tele2 created a sensation. Telia, on the other hand, got nothing.

All four winners had undertaken to provide coverage for at least 8.86 million people by the end of 2003. The licenses were to be valid until the end of 2015. The possibility was also left open for two or three of the licensees to build a joint network. In other words the number of ‘physical’ 3G networks could be reduced to two.

There was a great deal of speculation about the omission of Telia. Part of the explanation can probably be found in Telia’s failure to exploit the expertise within its organization about international license grants. Those who had been in the thick of things all around the world since the 1980s were never brought into the Swedish process and viewed Telia’s behavior in this context as “remarkably naïve,” to quote Telia’s Bo Magnusson.

The immediate effect of the PTS decision was for those involved to initiate negotiations with each other. On January 8, 2001, Telia and Tele2 announced their intention to cooperate on Tele2’s license. Two weeks later Europolitan and Hi3G stated that they were going to build a network together and later Orange was also included in this collaboration.

It soon transpired that none of the applicants had the capacity to build a 3G network at the promised speed. One of the conditions was that their 3G networks were to function by January 2002. They all admittedly managed this, but coverage extended only a few blocks beyond their head offices and the networks could be used by only selected members of their staff.

Author: Svenolof Karlsson & Anders Lugn