Gender parity and the global pandemic — ICT usage and opportunities

Senior Researcher, Consumer Insights, Ericsson Consumer & IndustryLab

Senior Researcher, Consumer Insights, Ericsson Consumer & IndustryLab

Senior Researcher, Consumer Insights, Ericsson Consumer & IndustryLab

Entering our eighth year of celebrating International Women’s Day here at Ericsson, I’m reminded of how much real progress has been made over the years. In countries throughout the world, women and young girls have achieved more equal access to healthcare, education, employment, and representation in business and politics. The trend seemed to be growing year after year — at least, this was the case until 2020. That year, all of our lives completely and abruptly changed. And the same was true for the progress toward gender parity in the world

In The Sustainable Development Goals Report by the UN Secretary-General’s office, the pandemic is referred to as “one of the worst international crises of our lifetimes.” Both COVID-19 and the prolonged, stringent restrictions (including national lockdowns) enforced as a result are expected to have long-term effects on households in terms of job losses, economic stress, mental and health-related challenges, and more. Amid all of this, it’s estimated that 70 percent of all healthcare and social workers are women, serving on the frontlines in the fight against the virus. women make up the largest demographic in professional sectors hardest hit by the pandemic. All of these factors have contributed to new and diverse challenges now standing in the way of progress for gender parity. And with the great societal shift that has seen our lives moved largely online, another disturbing fact has come even more starkly to light: Access to the internet and ICT devices — such as mobile phones, laptops, and tablets — is still not a given for women in many countries around the world.

In their Mobile Gender Gap Report 2020, GSMA found that among low- and middle-income countries (where the gender gap in mobile and internet access persists and is the highest), women last year were still 20 percent less likely to use mobile internet compared to men. This is an especially troubling statistic considering that access to mobile connectivity has been shown to accelerate social and economic development, yet around 300 million fewer women than men tend to access mobile internet, and women are 8 percent less likely than men to own a mobile phone.

Reading this, I’m reminded of an earlier project we at Ericsson launched in 2017 — before our latest 2020 study, which I’ll discuss soon — where we tried to explore and understand the ICT

gender gaps (the gaps in mobile internet use, device use, and service consumption) existing at the time in 32 selected countries. Back then, we discovered gender gaps in ICT use in all of the 32 countries, some driven by economic factors, some consumer life stage and working status, and others by culture and values.

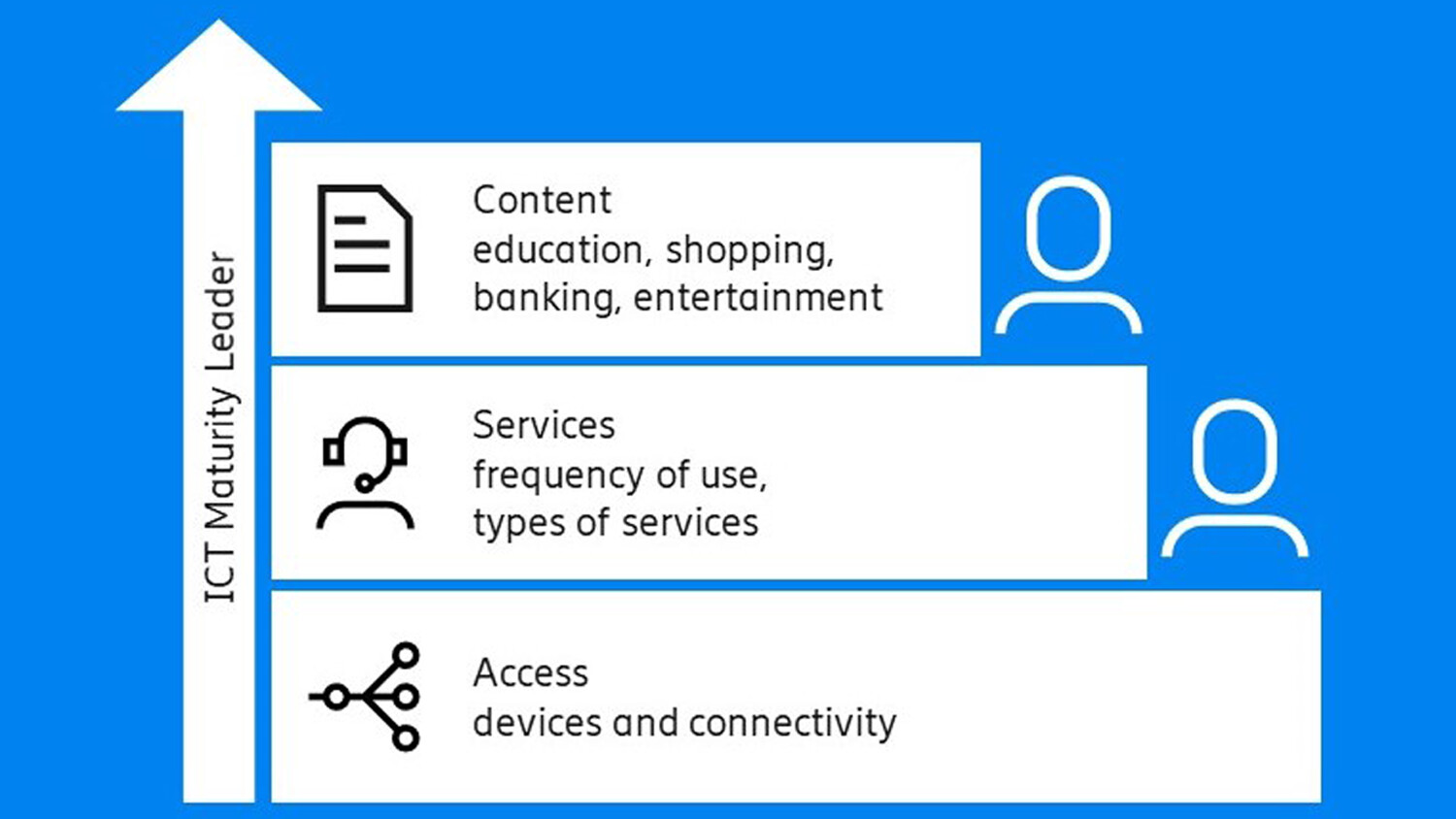

When examining this topic, it’s important to understand that simply providing access and affordable devices alone isn’t going to naturally lead to social and economic development — basic access entails basic use of services and apps. Rather, we think in terms of an ICT maturity ladder, where the full advantages of ICT devices and services may be unlocked only when one passes the services stage and enters the content stage. At the services stage, access to devices and connectivity can develop into habits of frequency and continuous use of different services across different devices. At this stage, we often see a gender gap manifesting itself in the form of a much narrower use of services among women than men. While on the last rung of the ladder, the gap is diminished or nonexistent and a broader use of devices, apps, and services (as well as overall similar online behaviors between women and men) becomes the norm.

Source: Ericsson ConsumerLab Analytical Platform 2020

But in 2020, we wanted to understand how the ICT gender gaps in the countries of our previous study had advanced since 2017, what the gender gaps looked like by December 2020, and what impact the pandemic may have had on the gender gaps after so many daily activities and habits were moved over to the digital sphere.

What we learned in 2017

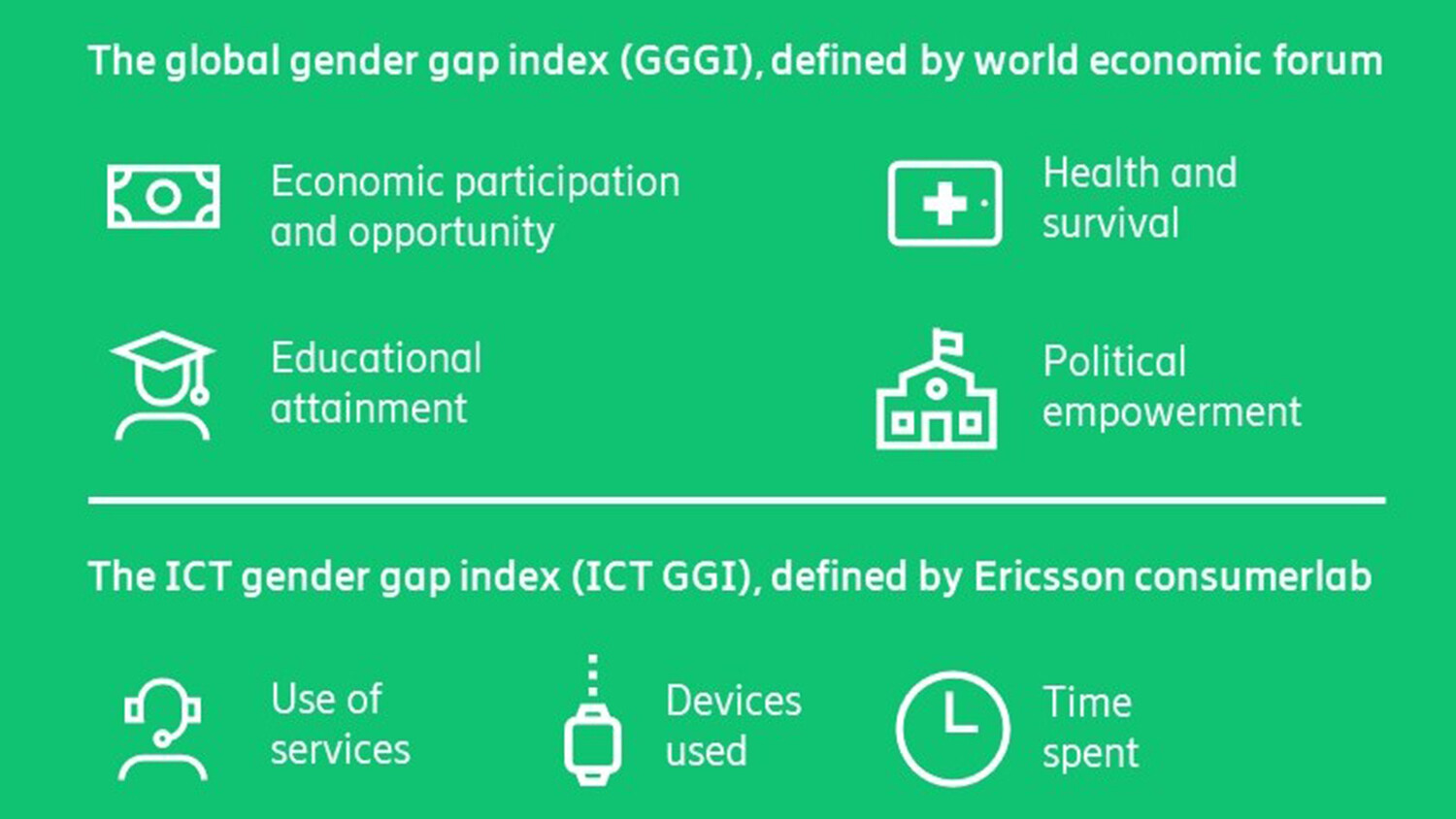

For our 2017 study, we built an ICT Gender Gap Index (ICT GGI) and measured the index value for our 32 countries. With a starting point of 0.00 (indicating low gender parity) and the ideal high value of 1.00 (gender parity achieved), the countries received various scores within this range. The challenge was that the index value alone didn’t give us an understanding of why it varied so much between the countries — even between countries we would have assumed would share a similar index value. So, we decided to map our own index against the Global Gender Gap Index (GGGI) of the World Economic Forum (WEF) to see if we could contextualize our findings.

Source: Ericsson ConsumerLab Analytical Platform 2020

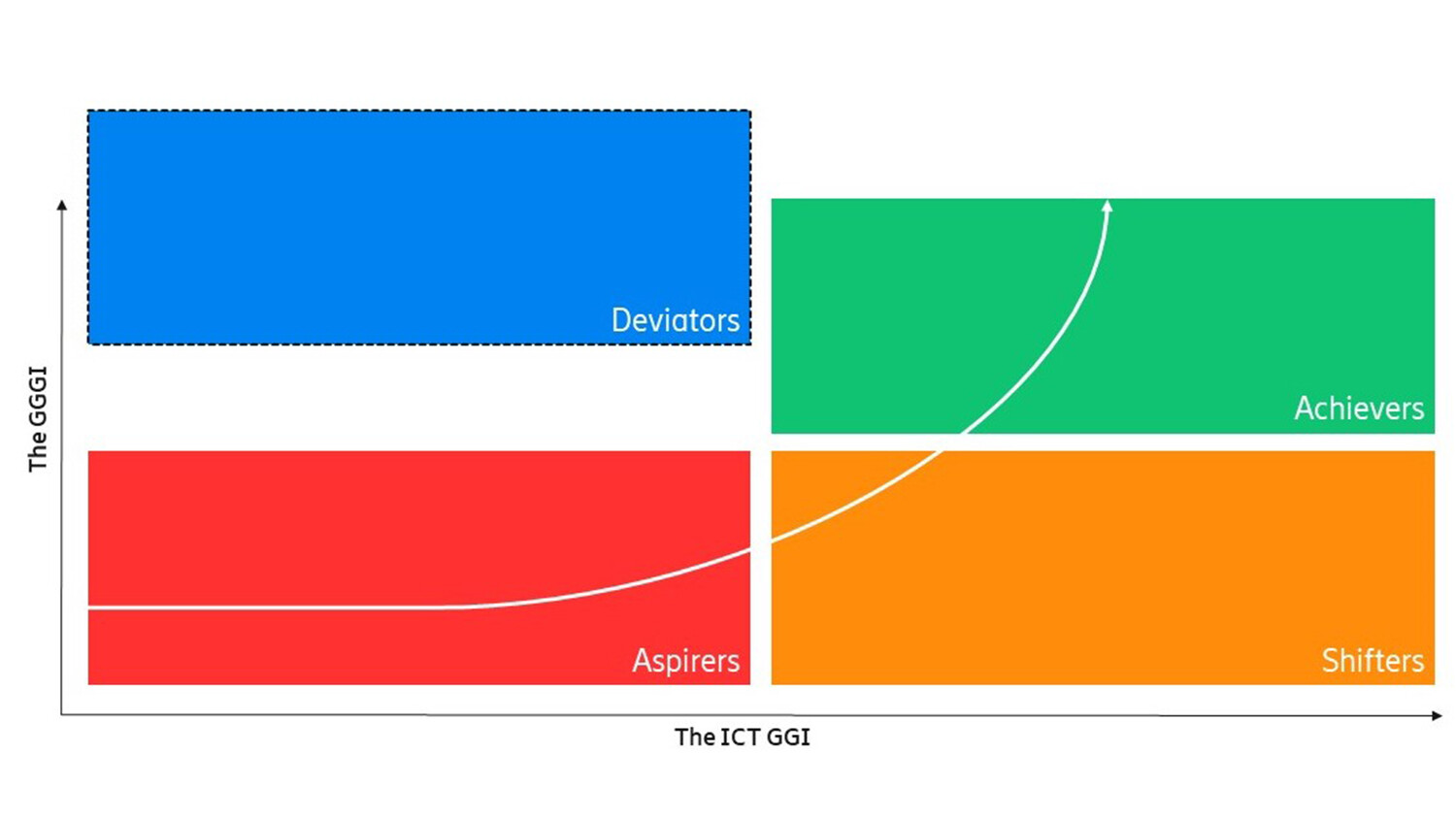

As we mapped these 32 countries in our ICT GGI and the WEF’s GGGI, we were able to form four different groups of countries showing similar patterns within the groups. Our ICT GGI values compared with the information on the state of gender parity across the four key societal pillars in the countries highlighted something important: There was a measurable relationship between our ICT GGI value and the WEF’s GGGI value.

Source: Ericsson ConsumerLab Analytical Platform 2020

We saw, for example, that among countries identified as achievers, the high ICT GGI value (indicating near gender parity in ICT usage) could be tied back to gender parity on the national level in terms of educational attainment, high economic participation, high rates of health, life expectancy, and (in some instances) high political representation in government. The reverse was also true: Countries identified as aspirers would have low ICT GGI values (indicating high gender gaps in ICT usage) across different consumer groups in the country while also having significant gender inequality across the four pillars of society. We did have a few deviating countries in our mapping, but the overall trend indicated that ICT gender parity in any given country could most often be seen as a reflection of equality in societies as a whole with regard to the equal economic, professional, and political participation as well as representation of women and men in society.

In a few developing markets in our study, such as in Thailand and South Africa, we observed a high ICT GGI value (despite low internet penetration among the overall population) coupled with low online presence and device usage among consumers as compared to other markets with similar index values. (The ICT GGI does not place any weight or value on aspects of economic or infrastructure advancements at a national level — it solely looks at gender parity among those already connected.) As a reflection of equality in societies as a whole, the uptake of ICT within a population appears to occur in a more equal manner (from a gender perspective) if there is an opportunity for it. Thus, achieving gender parity in ICT isn’t merely a question of whether or not there’s access to the technologies as such, but rather how consumers are able to adopt ICT based on individual circumstances and equal opportunities related to getting value from it.

What we saw in 2020

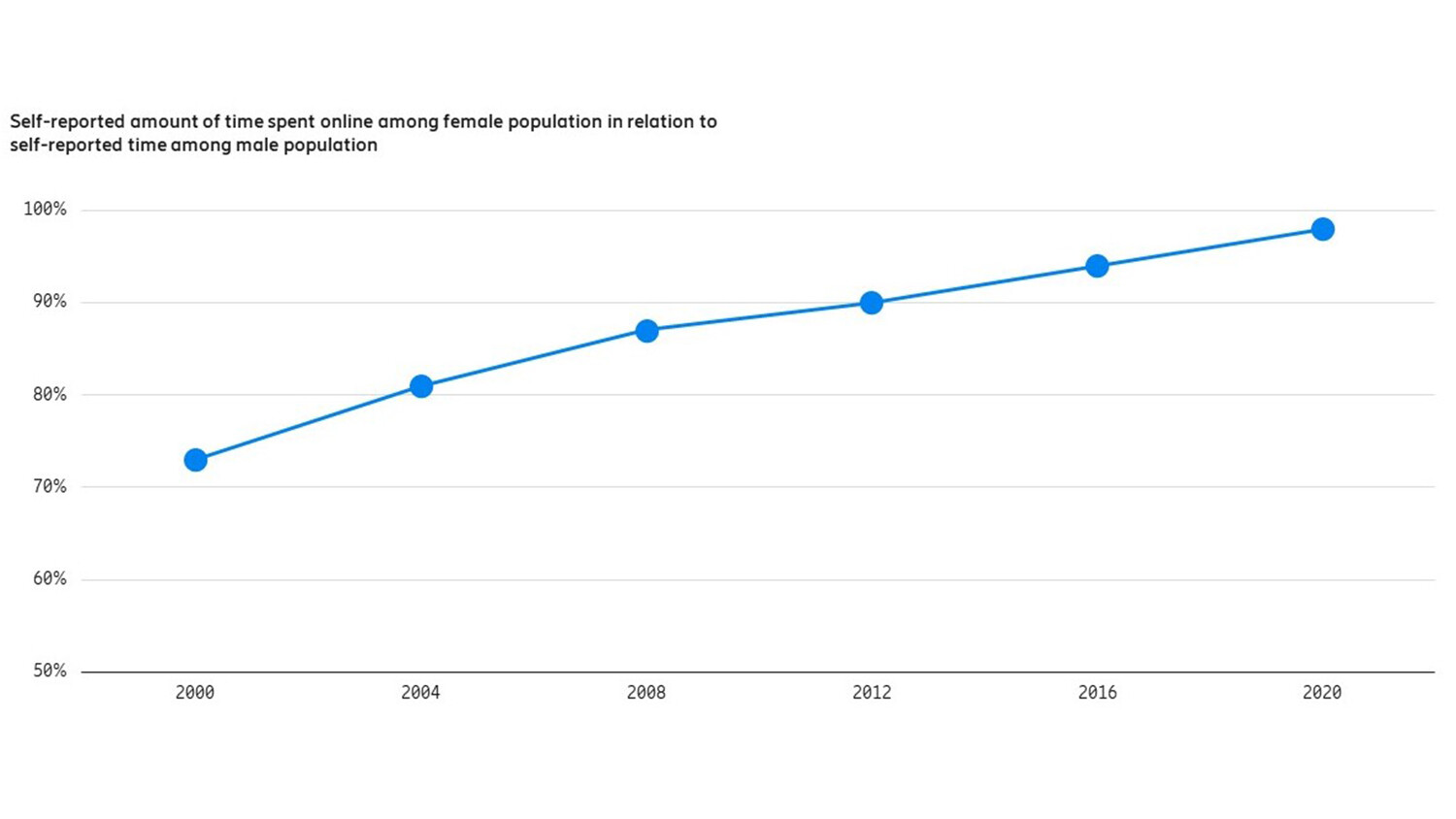

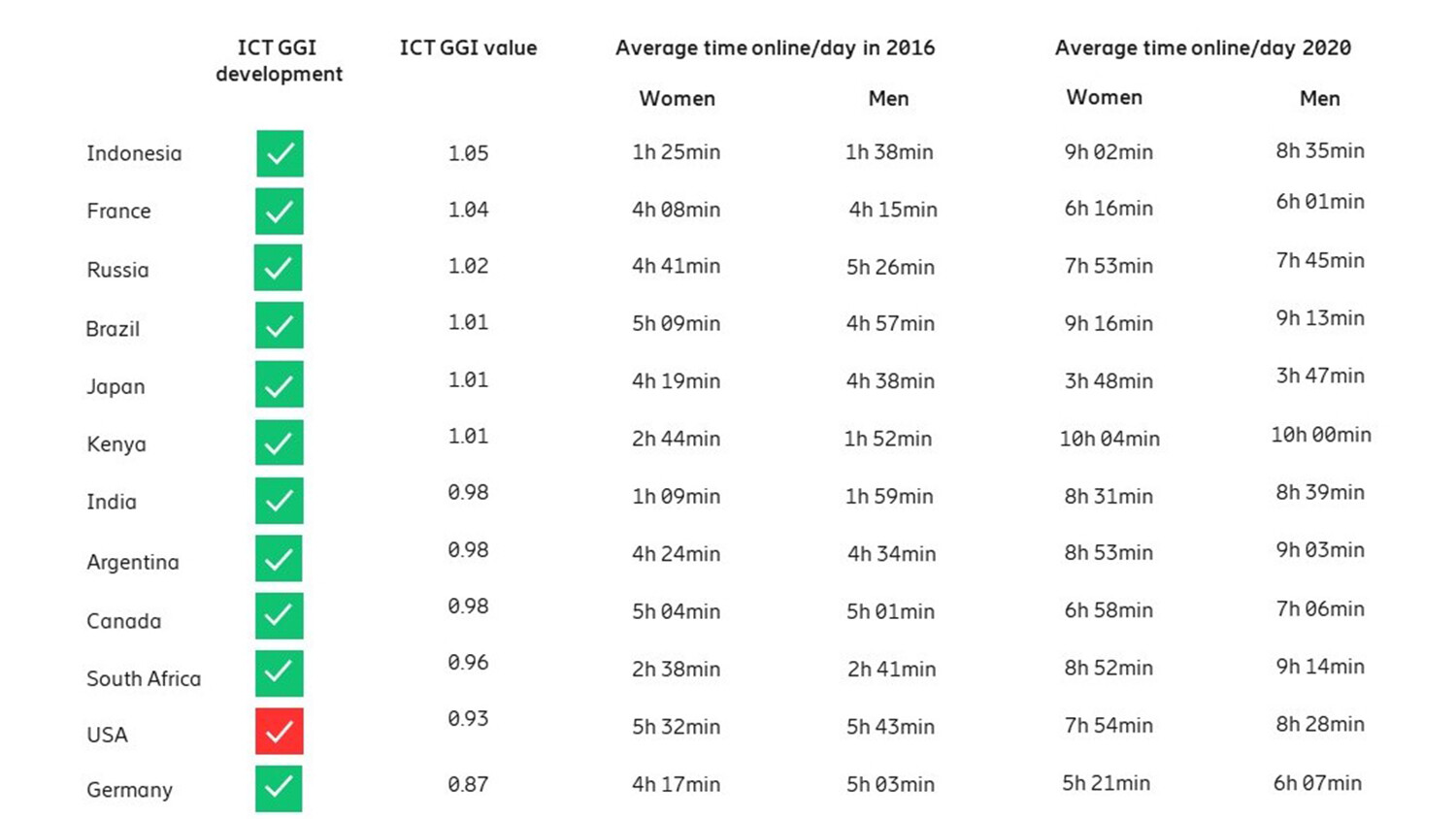

For our 2020 study, we decided to look at the ICT GGI values for 31 countries (23 of which were part of our 2017 study). For 21 of those 23, we had historical data which we could trace as far back as the year 2000, giving us a chance to see the broader development of the ICT GGI values for the 21 markets. Our first insight derived was that there was an overall positive trend towards gender parity in ICT during 2020. Comparing the 23 countries during 2017 and 2020, we also saw positive overall development reflected in higher ICT GGI values for nearly all of them (22, to be precise).

Base: Internet population aged 15–69 in 21 countries (Argentina, Australia, Brazil, Canada, China, Egypt, France, Germany, India, Indonesia, Italy, Japan, Mexico, Nigeria, Russia, South Africa, Spain, Sweden, Thailand, the UK, and the US)

Base: Internet population aged 15–69 within Argentina, Brazil, Canada, France, Germany, India, Indonesia, Japan, Kenya, Nigeria, Russia, South Africa, and the US

As access to connectivity and ICT continues to reach more consumers, and as usage advances among those already connected, we found another important marker of progress. In 2017, a 33-percent difference was found in ICT GGI values between the highest and lowest performing countries. In 2020, the difference was at 18 percent, indicating a closing of the digital gap among those already connected.

On a general note, an index value of 1.0 would indicate an achievement of gender parity in ICT for a specific country, and in a few of the 31 countries from 2020, this value was surpassed. In the best of circumstances, a score of 1.00 would indicate high levels of gender parity on a national level, but this, unfortunately, isn’t the case, which we see when looking at different groups in society.

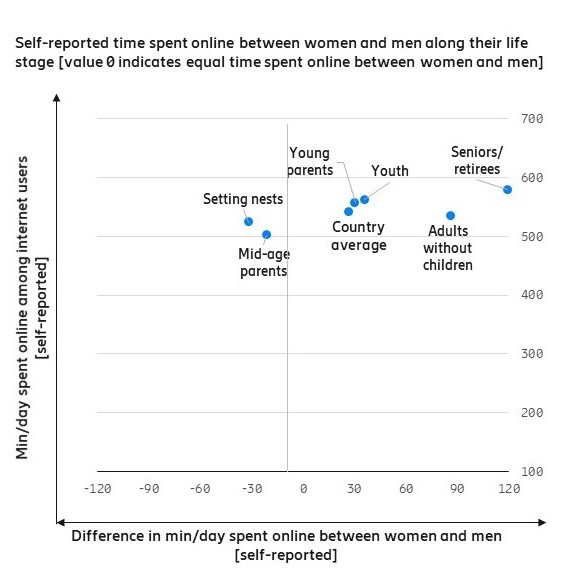

Base: Online population aged 15–69 within Indonesia

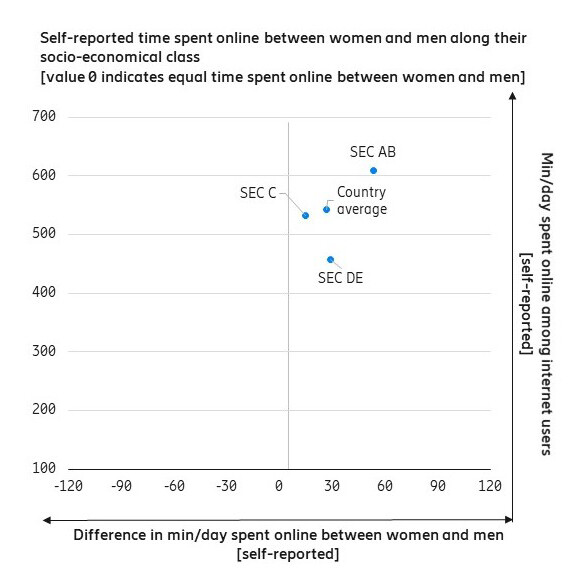

In Indonesia, for example — the country with one of the highest ICT GGI values — time spent online differs between genders when looking at life stages. Among seniors, adults without children, young people, and young parents, women are spending more time online than men. While in the case of those “setting nests” and middle-aged parents, there is still a gender gap of 31 minutes and 21 minutes, respectively, in time spent online. We interpret this to be driven by consumer life situations in their respective countries because, if we look at the economic classification of consumers in Indonesia and its impact on time spent online, we see that women still spend more time online than men. Though time spent online is only one aspect of ICT usage, the less time spent online does impact the time spent on different devices and the use of services.

Base: Online population aged 15–69 within Indonesia

Base: Online population aged 15–69 within Indonesia

With ICT GGI values varying significantly across the 31 countries from the 2020 study, and with differing progress on gender equality in society as well as development and access to telecommunications infrastructure between the countries, it’s important to see how online behaviors look in today’s world — especially looking back at 2020, when daily life abruptly changed.

Online life under the pandemic

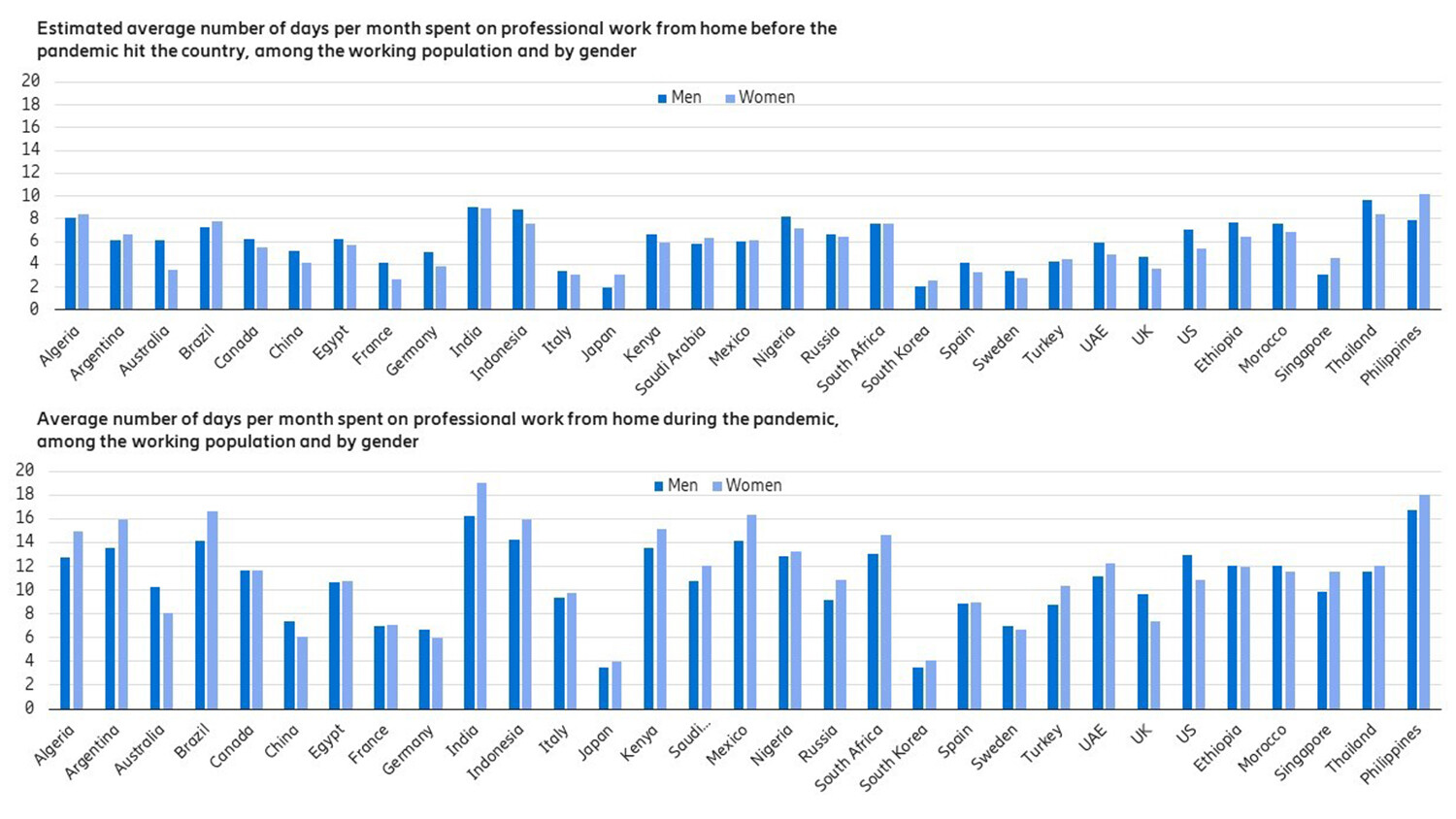

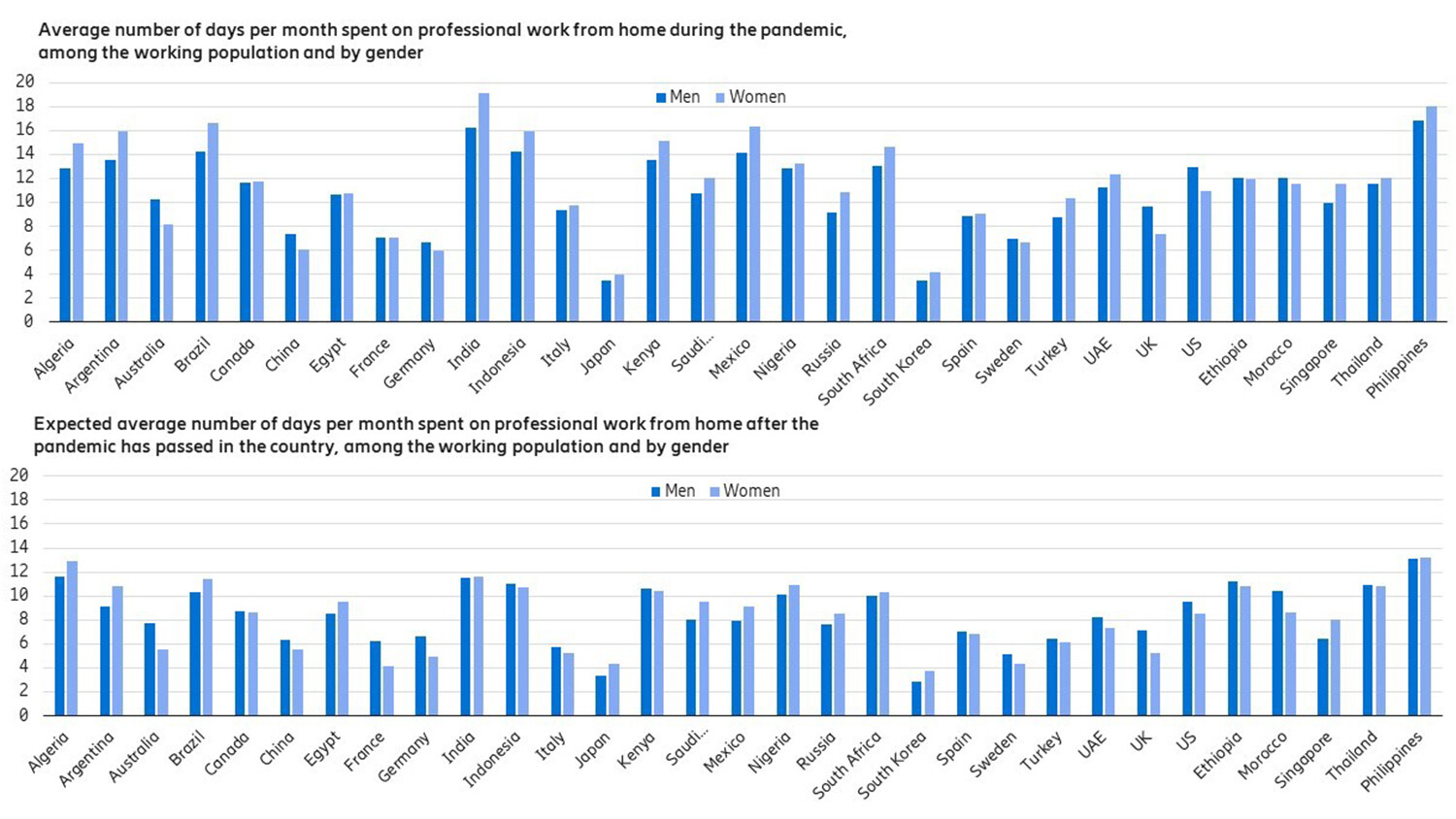

To understand just how much consumers shifted their daily habits during 2020, let’s look at what women and men reported in terms of the frequency with which they undertook a number of activities before the pandemic as opposed to during it as well as how often they expect to engage in these activities after the pandemic passes. Looking at the 31 countries on a national level to see the extent to which work life went online for the population in each country, we find the following:

Base: Online population aged 15–79 (69) years old within 31 countries (Algeria, Argentina, Australia, Brazil, Canada, China, Egypt, Ethiopia, France, Germany, India, Indonesia, Italy, Japan, Kenya, Mexico, Morocco, Nigeria, Philippines, Russia, Saudi Arabia, Singapore, South Africa, South Korea, Spain, Sweden, Thailand, Turkey, UAE, the UK, and the US)

Across all 31 countries and among both genders, working from home significantly increased during the pandemic. (It’s important to understand that in December 2020 — when this data was gathered — the countries were at various stages in their battles against the spread of COVID-19. The more severe the situation at that point in time was, the higher the reported frequency of working from home for both genders.)

Consumers across the markets indicated that they expect remote work to continue either at similar levels or to greater extents after the pandemic passes — not exactly as a new normal but more than before and with more women doing so than previously. This in itself is an important indication: Not only will many more consumers need to be able to work productively from home, but ICT tools and services will need to accommodate this for a higher share of the working population and for a diverse range of job types. Interestingly, countries with high ICT GGI values but where remote work was more commonly performed by men before the pandemic — such as Thailand (ICT GGI: 1.05), Indonesia (ICT GGI: 1.05), and Ethiopia (ICT GGI: 1.05) — saw an equalizing in the frequency of remote work for both genders during the pandemic. After the pandemic passes, it’s expected that the remote work gap in these countries will narrow or be bridged completely.

Countries with high ICT GGI values and higher frequencies of remote work among women than men — such as Argentina (ICT GGI: 0.98) and Brazil (ICT GGI: 1.01) — saw this gap maintained during the pandemic, and we expect it to remain after the pandemic passes. On the other hand, for countries with low ICT GGI values — such as Germany (ICT GGI: 0.87) and Australia (ICT GGI: 0.87) — the gap between men and women working remotely remained constant during the pandemic, and we expect it to remain even after the pandemic passes.

Base: Online population aged 15–79 (69) years old within 31 countries (Algeria, Argentina, Australia, Brazil, Canada, China, Egypt, Ethiopia, France, Germany, India Indonesia, Italy, Japan, Kenya, Mexico, Morocco, Nigeria, Philippines, Russia, Saudi Arabia, Singapore, South Africa, South Korea, Spain, Sweden, Thailand, Turkey, UAE, the UK, and the US)

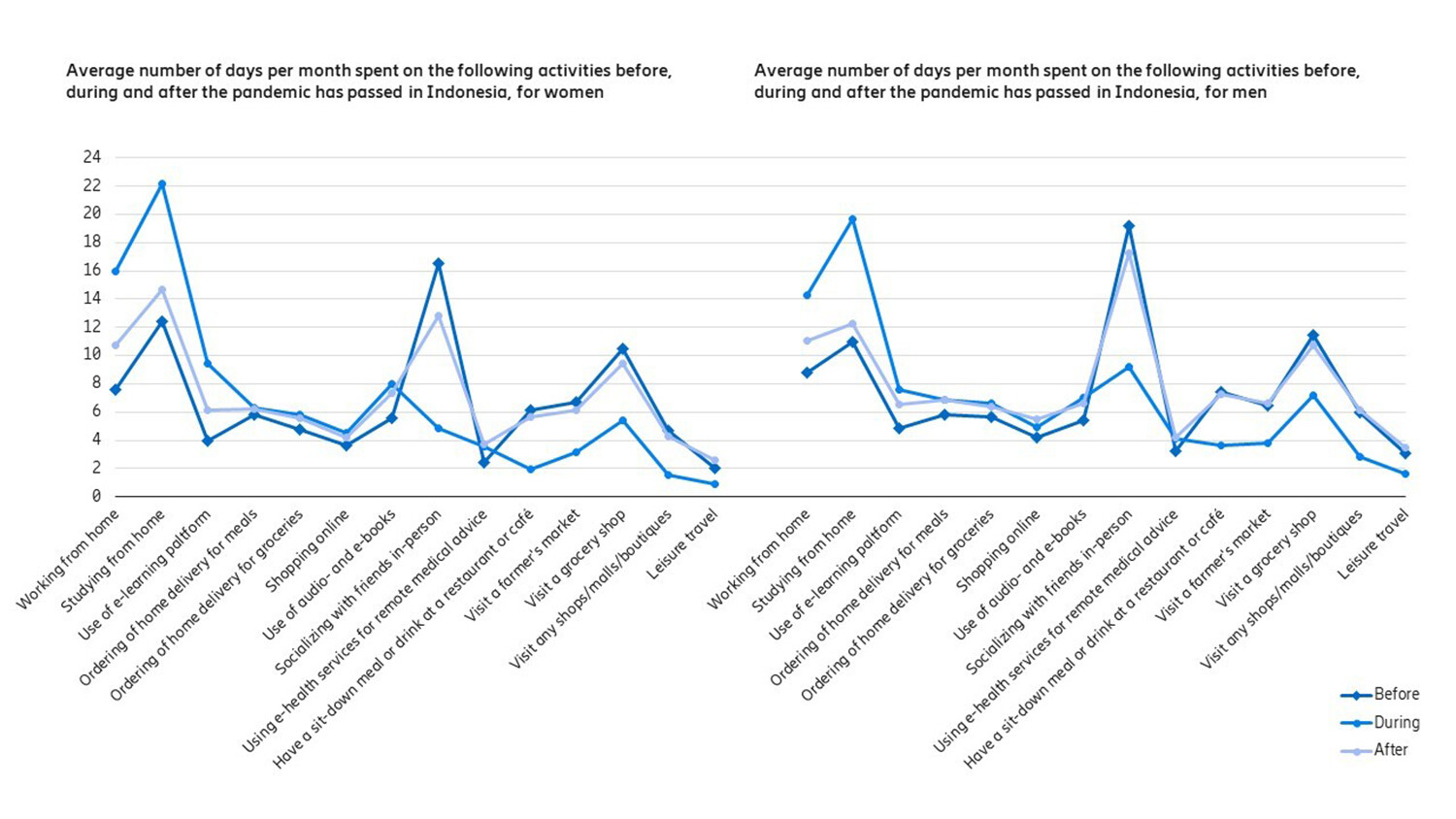

Looking at a range of daily activities in Indonesia in particular and how these have changed among women and men, there are a few indications as to what life after the pandemic might look like. The frequency of socializing with friends in person, visiting grocery shops, and — for women specifically — visiting cafés and restaurants is expected to decrease, while habits around shopping in stores, visiting farmers’ markets, and leisure travel are expected to return to normal. But it’s the online activities that best give us a glimpse of how digital behaviors will change going forward.

Base: Online population aged 15–69 within Indonesia

Both women and men indicated that they expect to engage in online activities more frequently after the pandemic passes compared to their usual habits prior to the pandemic. Interestingly enough, this isn’t simply a tendency among men and women in Indonesia on a general level, but — with very few exceptions — is a pattern that we see across different life stages in Indonesian society.

Base: Online population aged 15–69 within Indonesia

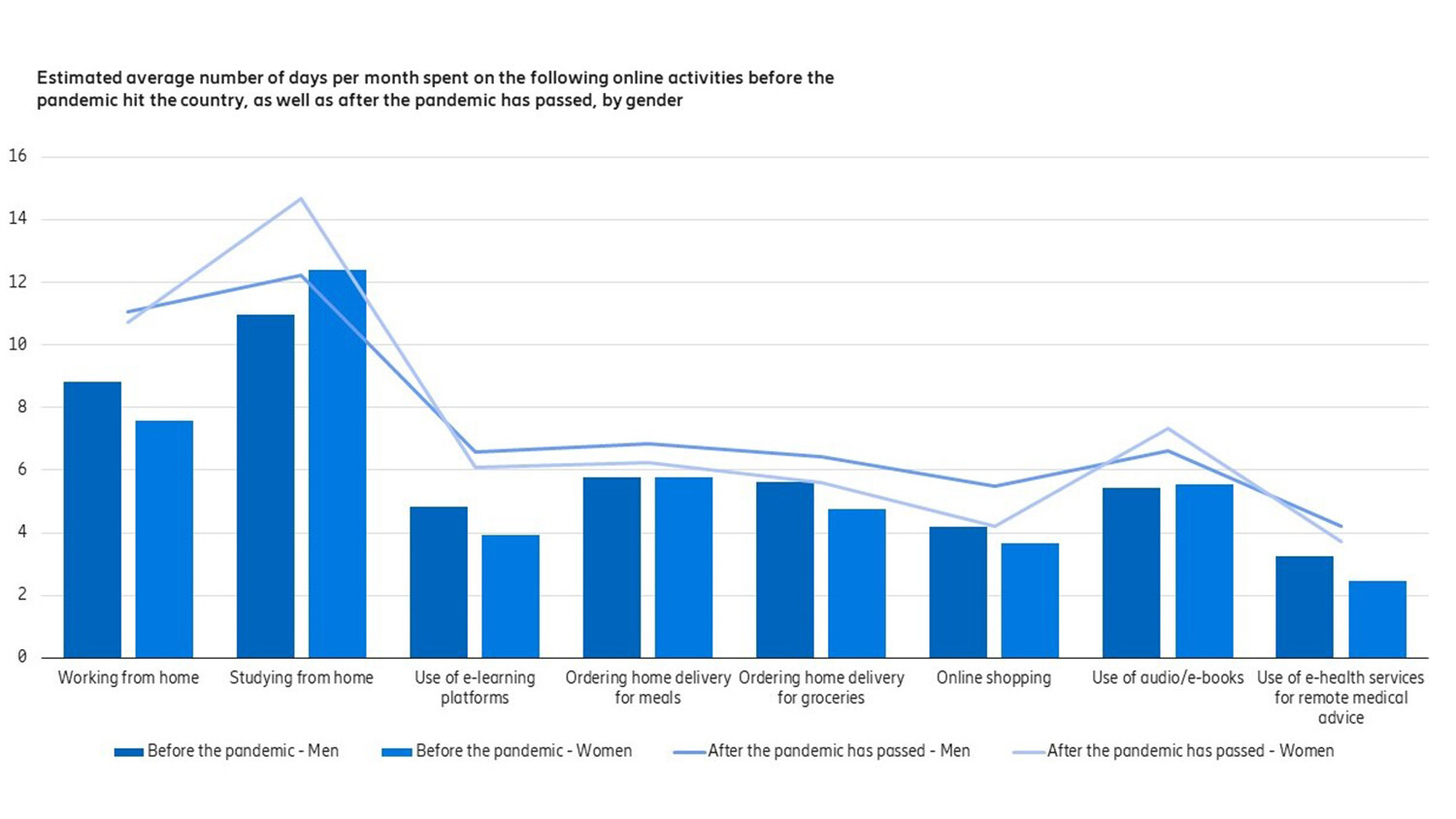

There are a few notable patterns that are important to highlight for the other 30 countries as well. In countries with ICT GGI values between 0.95–1.05, where women surpassed men in online habits related to (for example) remote working or studies even before the pandemic, we expect a reverse gap to remain after the pandemic passes. For the online activities in which gender gaps existed in these countries for a few online habits related to (for example) online shopping and the use of eHealth services, the gap is expected to decrease or narrow significantly. In countries with ICT GGI values between 0.90 and 0.95, and where gender gaps previously existed in terms of online activities, both women and men showed fewer differences in online habits during the pandemic, but we expect the gaps for a few online activities to narrow after the pandemic passes. In countries with ICT GGI values between 0.80 and 0.90 — such as Germany and Australia — the expectation surrounding future online behaviors only slightly impacts the existing gender gaps in a positive direction.

There is one important thing to remember when looking at habits surrounding ICT and the differing habits for consumer groups. How frequently consumers in general engage in online shopping varies across countries and depends on multiple factors. The sophistication and availability of eHealth services also differ greatly between countries as well as perspectives on how health and medical advice should be received. (Health is a particular area where culture has an impact on the perceived importance of physical — as opposed to digital — encounters with a physician.) Bearing this in mind, the benefits of exploring these habits and the future expectations surrounding them lies in understanding the patterns and tendencies that consumers demonstrate as well as how they may impact existing and future gender gaps in ICT.

What we’ve learned so far is that the pandemic not only increased online habits for both women and men last year, but that the increased utilization of connectivity and devices has also become a habit that will have a positive impact on gender gaps in ICT as we look toward a pandemic-less future.

Obstacles to gender parity in ICT usage

Having Indonesia as our example throughout this post helps us demonstrate the nature of the differences in how women and men use ICT. But we also need to understand the underlying drivers behind the gender gaps that are prevalent in the countries with low ICT GGI values. In 2017, we established that gender gaps in ICT usage tend to be driven by multiple factors, including maturity in ICT usage as well as culture and values. But the mapping of our own ICT GGI values against the WEF’s GGGI values for both Germany (ranked number 10 out of 153 countries) and Australia (44 among the 153) confused us. How is it that countries scoring so well on the WEF’s GGGI (which should indicate relatively strong gender equality in society) still indicate clear gender gaps in ICT usage?

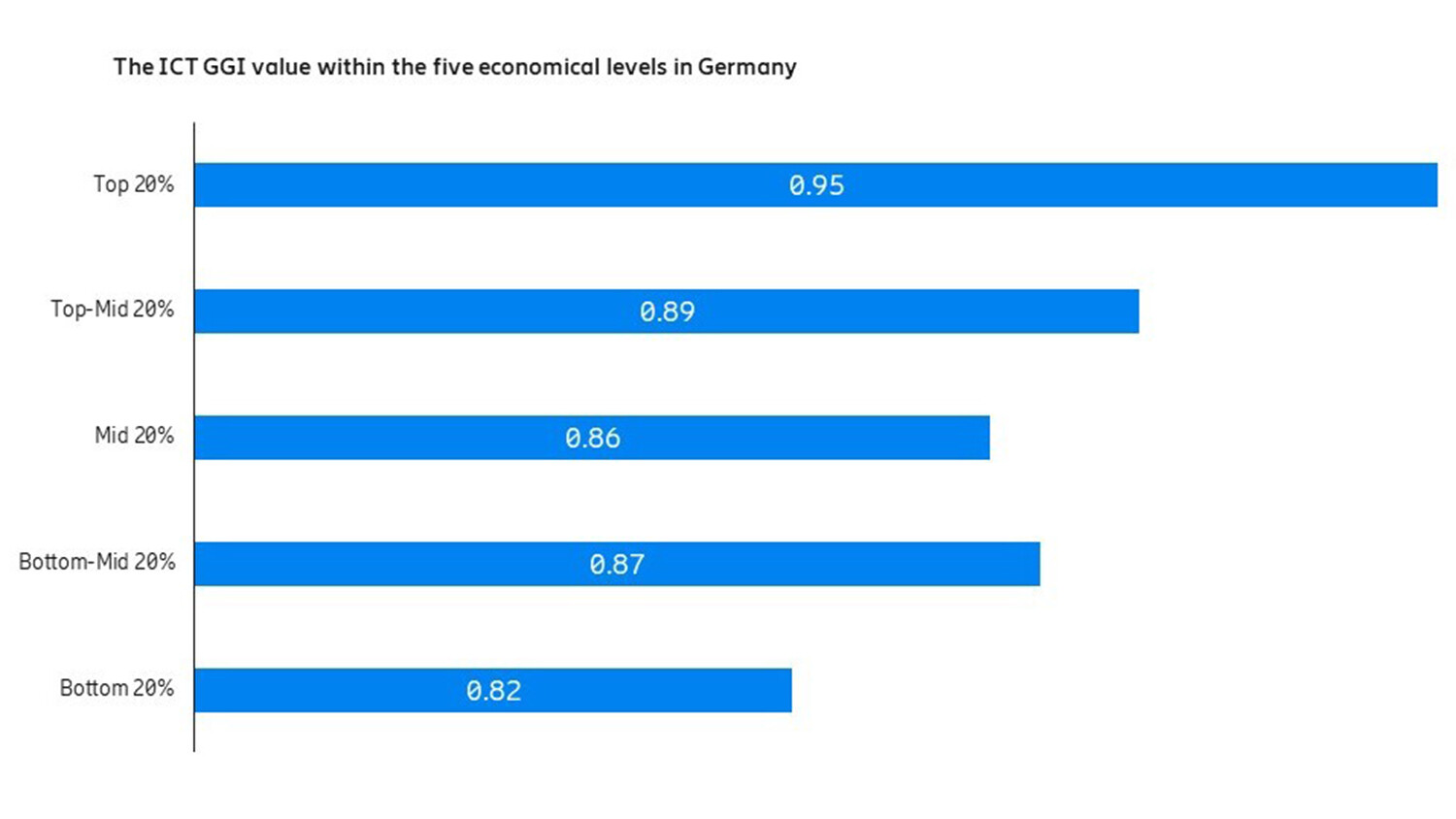

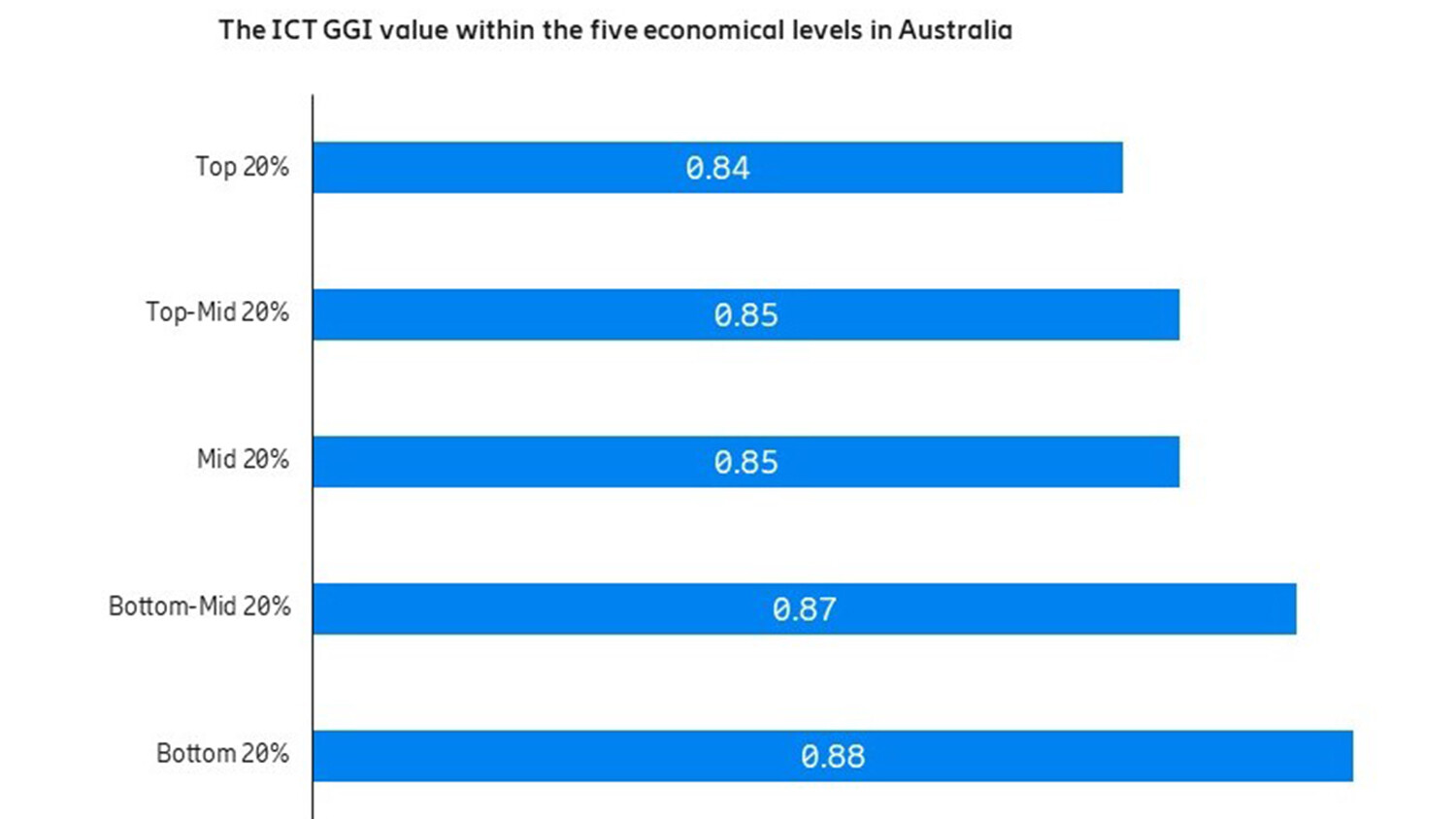

It all comes down to economy. Looking at the economic groups in Germany and dividing the population in five different groups based on income level, we see that the further down the economic groups wander, the lower the ICT GGI for the groups, indicating higher ICT gender gaps. Looking at the economic groups in Australia, we see similar patterns (with only minor exception).

Base: Online population aged 15–69 within Germany

Base: Online population aged 15–69 within Australia

Much in line with what the GSMA report states, a main barrier for both device ownership and online presence is affordability. With Germany and Australia, we see similar outcomes for countries on the lower end of the ICT GGI value ladder. This makes sense, knowing that access to ICT devices, services, and connectivity doesn’t automatically make taking full advantage of the capabilities possible if costs are an issue.

An opportunity worth exploring

Discovering these positive findings on ICT usage, even amid the new gender parity setbacks posed by the pandemic, is reassuring. All in all, it seems that, since 2017, there has been meaningful progress both in closing existing gender gaps in ICT usage as well as reaching gender parity within certain consumer groups across societies. With continued efforts and heightened awareness, the future may hold even more progress as we move away from this global pandemic and can restart different parts of daily life that have been limited by our current situation.

While women and men may always have diverging online behaviors due to personal interests, professions, and hobbies, the differences should be dictated by these factors rather than socio-economic limits. The analysis we’ve conducted here points to the fact that in the face of a new normal with limited physical mobility and interaction, the online habits of women and men aren’t, in fact, so different after all, and they’re dictated by factors beyond access alone. This is where achieving greater gender equality will have a big role to play in the speed at which ICT gender parity reaches all. And that’s an opportunity worth exploring.