Mobile money - six ways in which the ecosystem is evolving (part 1)

Head of Mobile Financial Services

Product Marketing Manager, Business and Operations Support Systems

Head of Mobile Financial Services

Product Marketing Manager, Business and Operations Support Systems

Head of Mobile Financial Services

Product Marketing Manager, Business and Operations Support Systems

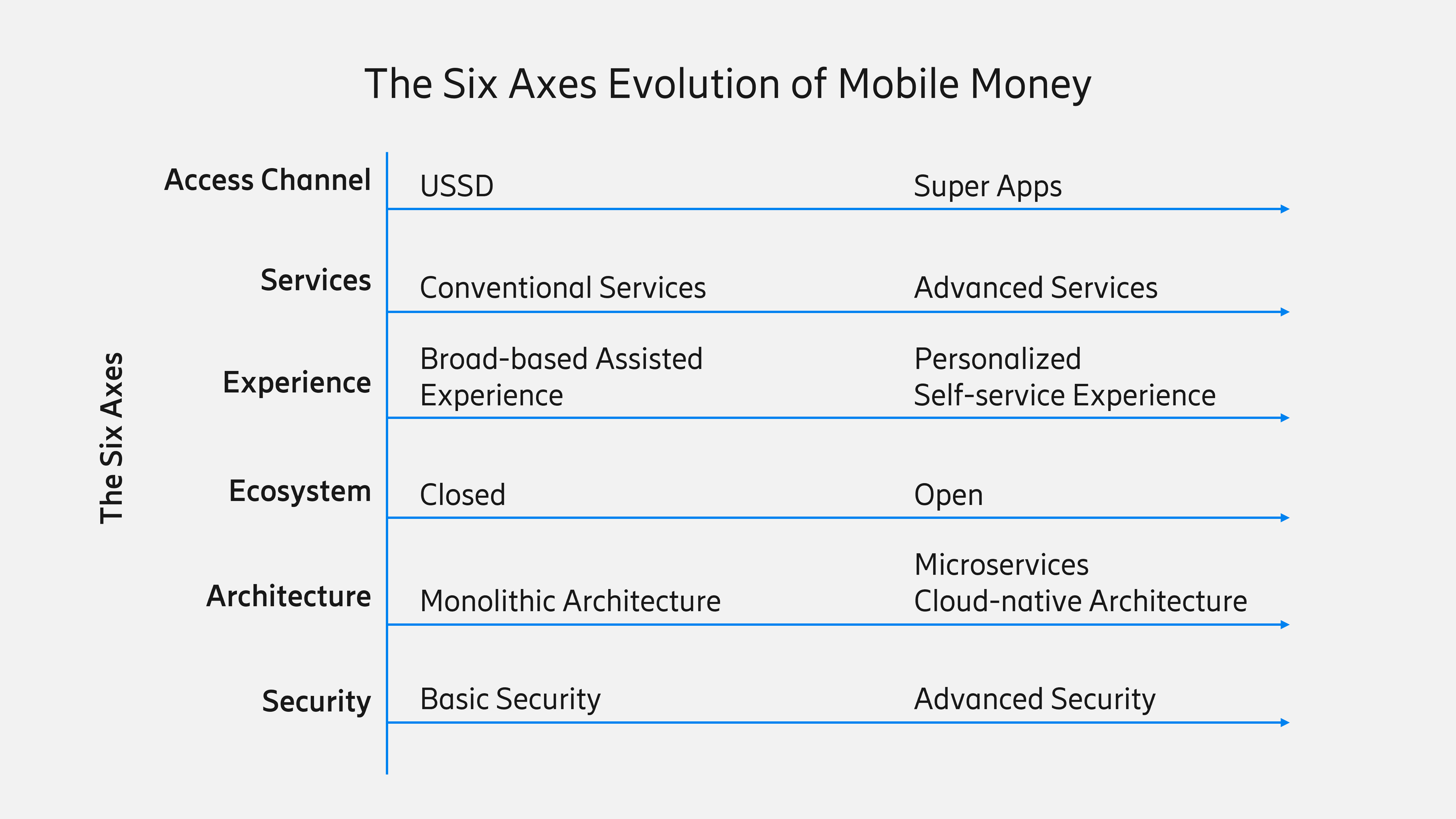

It wouldn’t be an understatement to say that in the financial services industry the last decade has belonged to mobile money, and the data from GSMA corroborates it. Mobile money services have doubled over the last 10 years, from 169 services in 71 countries in 2012 to 316 services in 98 countries in 2021. Mobile money registered customers have grown tenfold from 134 million in 2012 to over 1.35 billion in 2021, and transactions have multiplied over 14 times from USD 68 billion in 2012 to more than USD 1 trillion in 2021, making mobile money one of the fastest growing branches of the financial services industry. Mobile money’s upward growth trajectory is expected to continue in the next decade as well. The entire mobile money ecosystem is evolving at a rapid pace. To capture and understand the expansion of the mobile money industry, let’s look closely at the six axes on which this industry is evolving—access channel, services, experience, ecosystem, architecture, and security.

1. Access channel axis evolution: From USSD to Super App

At its outset, the objective of mobile money was to provide financial services to unbanked consumers in emerging countries. The target consumers were those who had basic mobile phones or feature phones. Hence, mobile money providers chose device agnostic access channels, such as, Unstructured Supplementary Service Data (USSD), SIM Application Toolkit (STK) and Interactive Voice Response (IVR) for offering mobile money services. USSD, a session-based text communication channel, became popular due to its easy and cost-effective accessibility and familiarity. In Africa, which houses more than half of the world’s mobile money services, 90 percent of mobile money transactions were conducted through USSD till 2018. However, USSD doesn’t deliver the best experience as a session involves navigating multiple screens, which is time-consuming and cumbersome for consumers.

The mobile phone landscape is changing quickly. The availability of cheaper smartphones, reduced data costs and the advent of pay-as-you-go-device schemes is fueling the adoption of smartphones. A case in point is Africa, where till 2018 only 40 percent of mobile phones were smartphones, as per GSMA Intelligence data. This has now grown to 56 percent in 2022 and is expected to jump to 87 percent by 2030. Mobile money providers are as a result feeling encouraged to introduce mobile money apps and promote their usage.

Mobile money apps enhance the user experience significantly, as it’s easier to navigate an app compared to the USSD menu. All transaction information like the recipient’s mobile number, transaction amount and transaction purpose can be entered in a single screen of the app, speeding up the transaction. Mobile money apps integrate with phone’s contact list; hence, the customer doesn’t need to type the recipient’s mobile number manually, reducing the transfers to wrong number due to typing errors. Many mobile apps also provide biometric logins, making mobile money services more secure. Mobile money apps also facilitate QR code-based money transfers and merchant payments. QR codes simplify and speed up transactions, as they eliminate the need to enter the recipient’s or merchant’s number. An analysis from GSMA showed that merchants that use QR codes transacted three times more in value than merchants using other channels. Mobile apps support dynamic user journeys, the creation of personalized profiles including adding photos and selecting background themes, in-app notifications sharing one time passwords (OTPs) and marketing messages, entering information like card details to load mobile wallets, customer care chats and call buttons, and much more.

And now, mobile money apps are evolving to super apps. A super app is a one-stop-shop that provides access to multiple services through a single interface. Services like e-commerce, travel and ticketing, credit, insurance, healthcare bookings and entertainment are built as mini programs or mini apps within the super app. Super apps eliminates the need to download various apps and remember multiple passwords, optimizing phone memory and enriching the user experience.

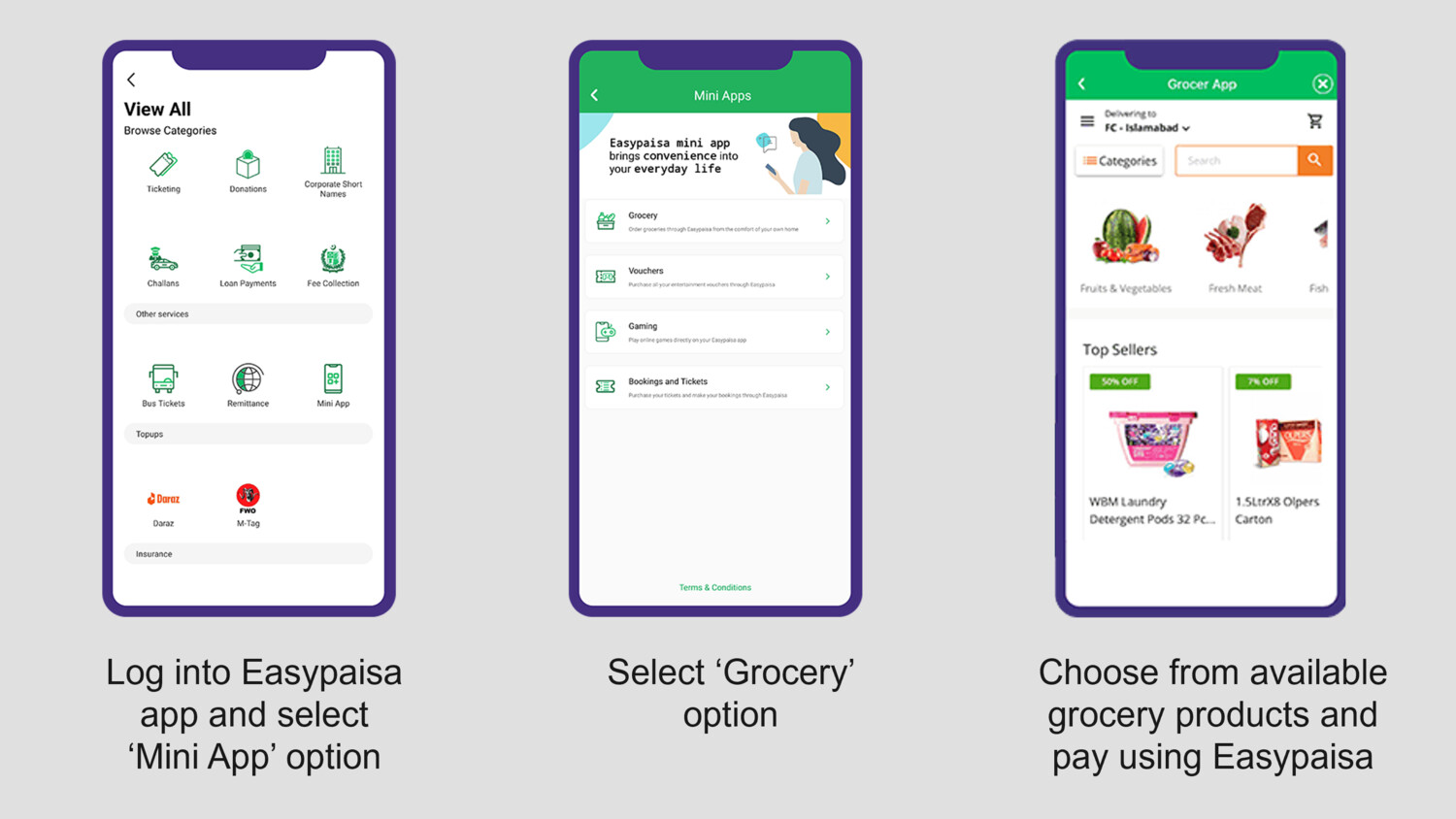

Let’s take the example of the leading mobile wallet app in Pakistan, Easypaisa, which has embarked on the journey of becoming a super app. Easypaisa hosts multiple mini apps such as GrocerApp (grocery shopping), BookMe (ticket purchase), Gamebox (gaming) and Tapshop (voucher purchase). It provides a seamless user experience, as the entire transaction journey from selecting products to making payments and receiving rewards takes place within a single app. For example, to buy groceries, the user logs into the Easypaisa app, taps on the mini app option, selects GrocerApp, chooses from available grocery products and checks out by paying with Easypaisa, all within a continuous user journey in a single app.

Image source: easypaisa.com.pk

Other data-based mobile money access channels that are coming up on the horizon are web, chatbots, voicebots and wearables. Chatbots and voicebots can be used for multiple purposes like onboarding consumers, responding to consumer queries, performing financial transactions and providing consumer support. They leverage rule engines, artificial intelligence (AI) and natural language processing (NLP) to process human language, understand its meaning and recognize the intent and sentiment to provide an appropriate human-like response for meaningful conversations. They are available 24/7 and can be hosted on mobile money apps, websites or social media platforms like WhatsApp and Facebook Messenger.

Wearables are supporting low value, high frequency transactions, for example, taping smartwatch with near-field communication (NFC) payment capabilities at metro train turnstiles multiple times a day to make payments for train travel. In the future, IOT devices will open up the connected payments space to include automated payments by smart home appliances, in-car payments at parking and toll booths, and automated payments by smart electricity meters, and so on.

2. Services axis evolution: from conventional to advanced services

The most notable catalyst for the introduction of mobile money has been the need for quick and cost-effective money transfers for migrants. In many emerging countries, people migrate from rural and peri-urban areas to urban areas for work and send money back home to feed their families. However, due to a lack of formal financial infrastructure, in the past people had to use risky, cost-incentive and timely informal channels such as requesting bus drivers to send money back home. Mobile money provided a fast, secure, and cost-effective alternative of transferring money. Hence, person to person (P2P) transfers along with last-mile services of deposit and withdrawal at mobile money agents became the primary mobile money use-case. Mobile money providers also provided utility payment services like electricity payments, water payments and mobile top-up services.

Mobile money providers were not satisfied with the cash-in, transfer and immediate cash-out of the money. They wanted to increase the money coming in and retain the money in the mobile money system to boost transactions and increase the float interest. Hence, mobile money providers introduced inward international remittances and bulk payments like financial-aid disbursements and salary payments to increase the value of money entering the mobile money platform. Mobile money providers also on-boarded and added merchants into the ecosystem and introduced various merchant payment services to retain and circulate the money in the mobile money platform. Today, rather than cashing-out money, more and more consumers are paying digitally at both physical and online merchants covering shopping to betting, taxes to tolls and school-fees to pay-as-you-go solar payments.

With consumers’ basic money transfer and payment needs met, mobile money providers further improved consumers’ lives by offering advanced financial wellness offerings like savings, loans, overdrafts, the option to buy items on credit, buy now pay later (BNPL) services, and insurance and investment services. Mobile money providers launched innovative financial services like no-frills small savings accounts, short-term micro-loans with rule engine-based credit decisioning, micro-insurance based on mobile money transactions and robo-advisory supported investment services. These services are designed on the ‘finance for all’ proposition and cater to both banked and unbanked consumers using mobile money. These services have been carefully crafted to comply with regulatory conditions and transaction limits.

Take the example of MTN Mobile Money (MoMo), Africa’s leading mobile money service available in more than 15 countries. MTN has launched a full suite of advanced mobile money services in the last few years to diversify its service mix and grow transactions and revenue per user. MTN MoMo provides MoKash savings and loan services. MTN MoMo users can open a MoKash savings account instantly from their mobile phone, without any paperwork. MoKash is a no-frills account with no ledger fee, no minimum balance requirement and zero transaction charges for moving money between MoKash and MTN MoMo accounts. Consumers can schedule automatic savings with an auto-save feature. Consumers can also apply and get small-value short-term (30 days) micro-loans immediately through their mobile phone. The credit limit is calculated, by a rule engine, based on a number of factors like the consumer’s usage of MTN voice, data and mobile money services as well as the length of time the consumer has been on the MTN network. MTN also offers MoMo-Advance, an overdraft service, allowing MoMo users to complete their transactions when they do not have sufficient funds in their MoMo wallets. MTN has also introduced aYo insurance, which provides life and hospital cover to the value of triple the amount transferred by the user in the last four months using MTN MoMo. MTN also provides investment and pension services in some countries.

The usage of MTN MoMo advanced services is growing rapidly. MoKash provided loans worth USD 100 million on average monthly in 2021 compared to USD 77 million in 2020. aYo insurance had 6.6 million active users and MoMoPay merchant payments processed transactions valuing USD 13.3 billion for over 785,000 merchants in 2021. Overall, MTN MoMo advanced services contributed 23 percent to MoMo group revenue in 2021, up from 16 percent one year ago (Source: MTN 2021 Annual Report). Similar trends are seen in country operations like Uganda (see image below).

For MTN Mobile Money Uganda, between H1 2021 and H1 2022, the revenue contribution from advanced mobile money services has grown from 14% to 25%

H1 2021: MTN Mobile Money Uganda Revenue Split

H1 2022: MTN Mobile Money Uganda Revenue Split

Hence, advanced services are helping mobile money providers to reduce dependence on conventional money transfers, cash-out revenue and also fight competition emerging from new fintech start-ups entering the market with low or zero service fees.

The future of mobile money looks interesting with the buzz around central bank digital currencies (CBDCs) and digital assets growing. Mobile wallets will be expected to facilitate digital currency and digital asset transactions in the future, in addition to the digital payments they facilitate today. Automated payments by connected devices (IOT payments) and increased use of robo-advisors in investment services will add another layer to the mobile money service mix.

3. Experience axis evolution: from broad-based assisted experience to personalized self-service experience

When mobile money was introduced, consumers required education and support to use mobile money services. Mobile money providers offered complete assistance through agents and consumer support staff to gain consumer confidence. Agents not only helped consumers to register for mobile money services and perform last-mile deposit and withdrawal transactions, but they also performed transactions like money transfers for them. These assisted transactions are called over-the-counter (OTC) transactions. Consumer support staff helped to resolve consumer issues like resetting blocked pins or reversing transfers to wrong numbers.

As mobile money adoption increased and consumers gained confidence in using it, providers stimulated the shift from assisted to self-service mode. A key illustration of self-service is digital Know Your Customer (KYC) and self on-boarding. Consumers today can quickly register for mobile money anywhere, anytime; by

- downloading the mobile money app

- entering their mobile number and confirming it using an OTP

- inputting personal details

- clicking and uploading the photo of their identity documents

- capturing their selfie for photo proof

- setting up a PIN to complete the digital registration

Multiple technologies are helping to make the digital self on-boarding process both seamless and secure. Optical character recognition (OCR) is used to scan identity documents and convert them into machine readable text, to verify the consumer’s identity. 3D selfie technology and liveness detection checks that a person is present live during the KYC and is not spoofing the system using a static image. AI and deep learning-based face matching technology verifies that a consumer’s selfie matches their photo in the identity document. Geolocation capture ascertains that the user is in a permissible location and not in a foreign country, while anti money laundering (AML) software prevents barred people from registering for mobile money services.

Other examples of a shift toward self-service mode are a reduction in OTC transactions and automation of key consumer queries handled by consumer support staff. Consumers can themselves reset blocked pins or passwords by answering a secret question and reverse transfers to a wrong number with the consent of the recipient, and without the help of consumer support staff. This not only improves consumer experience but also reduces consumer support traffic and optimizes costs for the mobile money provider.

The biggest shift is toward consumer experience personalization. Initially all consumers were treated as a single monolithic block, but now, based on parameters such as KYC profile (partial KYC or full KYC) and transaction history, consumers are segmented and graded to receive differentiated experiences. Based on grade, consumers are allocated services, transaction limits, rewards, and benefits.

Personal finance management (PFM) tools are being provided to consumers for a more personalized experience, empowering them to not just carry out transactions but also control their spending and budgets. PFM helps mobile wallet users to have aggregate views of money inflows and outflows through visual dashboards. Consumers can set budget limits and alerts for expenditures under different categories like transport, education fees, food and dining, utility payments, and entertainment, and compare their expenditures with previous months to manage their finances better. Consumers can also set personalized payment alerts to avoid missing due payments or meet their financial goals. PFM tools leverage data analytics, rule engines and AI algorithms to forecast future money inflows and outflows and provide personalized recommendations on savings and investments.

Data analytics, rule engines and AI are also being used for credit scoring and to provide personalized offers. Data analytics software analyzes multiple consumer parameters such as age, occupation, income, length of time consumer has been on mobile network, mobile usage, mobile wallet average balance, transaction history, payment patterns and more to provide a unique credit score to each consumer. This credit score is generated using alternative data sources and is used to provide instant micro-loans to consumers including unbanked ones without any credit history. Mobile money providers are partnering with enterprises and merchants to offer personalized offers and discounts, based on customer location, transaction history, payment patterns, and so on.

Rewards and loyalty programs are also embracing personalization. Instead of providing fixed rewards or cashback on registration and transactions, mobile money providers are experimenting with gamification to engage customers. Gamification techniques like winning a scratch card after every transaction to receive cash-back or spinning a wheel after every few transactions to get new rewards, rouses customer curiosity and ensures frequent app visits and repeat transactions. Gaming techniques such as badge collection (wining badges after each transaction and having the option to complete a set) or leader boards (accumulating points after each transaction and featuring on leader board) bring in a playful competitive spirit between consumers and their peers, while accelerating transaction growth.

To be continued - In second part of this two-parts blog series, we will read about the other three axes of mobile money evolution - ecosystem, architecture, and security.

Read part 2 of this blog series here

Related content

Read about Ericsson Wallet Platform

Read our Ericsson Perspectives article: The future of money: How digital ecosystems are changing our understanding of value and trust

Read the report on mobile money in Sub-Saharan Africa Mobile financial services on the rise (pdf).

Read more:

- Explore IoT