Mobile money - six ways in which the ecosystem is evolving (part 2)

Head of Mobile Financial Services

Product Marketing Manager, Business and Operations Support Systems

Head of Mobile Financial Services

Product Marketing Manager, Business and Operations Support Systems

Head of Mobile Financial Services

Product Marketing Manager, Business and Operations Support Systems

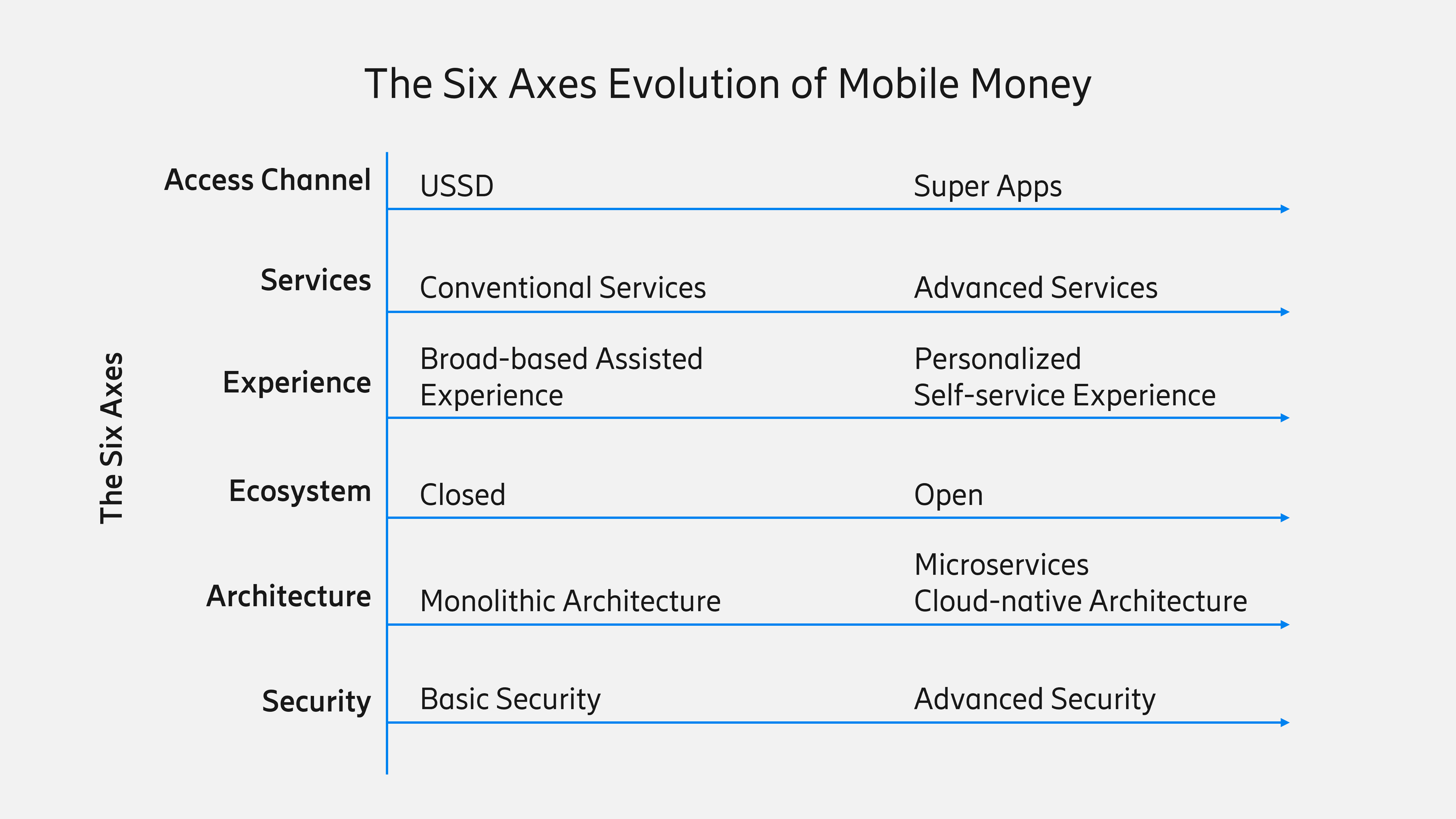

In first part of this two-parts blog series, we read about the first three axes of mobile money evolution – access channel, services, and experience. In this part we will focus on the other three axes - ecosystem, architecture, and security.

4. Ecosystem axis evolution: from a closed to open approach

Mobile money services started as closed loop services where consumers could transfer money only to other registered consumers or make payments only to registered merchants in the system. Mobile money providers acknowledged that to harness the full potential of mobile money they would have to break the silos and become interoperable and open to integrations. As a first step, mobile money services connected with each other through bilateral integrations or switches to enable domestic interoperability between mobile money services within a country. Then, mobile money providers partnered with banks and financial institutions to enable transfers between bank accounts and mobile wallets and together launch mobile money-based savings, loans, overdrafts, and other banking services. Thus, mobile money providers established a complementary rather than competing association with banks. As per GSMA, today, in more than 48 countries consumers can transfer money between accounts held by different mobile money providers and financial institutions.

Mobile money providers also integrated with money transfer operators (MTOs) like Western Union, MoneyGram and WorldRemit and remittance hubs like MFS Africa and TerraPay to facilitate inward and outward international remittances. For example, Etisalat has partnered with MoneyGram allowing e& money wallet users in the UAE to transfer money to over 200 countries and territories. Users can opt from bank transfers, wallet transfers or cash pick-ups to transfer money. In Africa, MTN MoMo Uganda users can make instant wallet-to-wallet money transfers to MTN MoMo users in Rwanda, M-Pesa users in Kenya, EcoCash users in Burundi and Airtel Money users in Tanzania. MTN MoMo facilitates more than 144 international remittance corridors in eight countries.

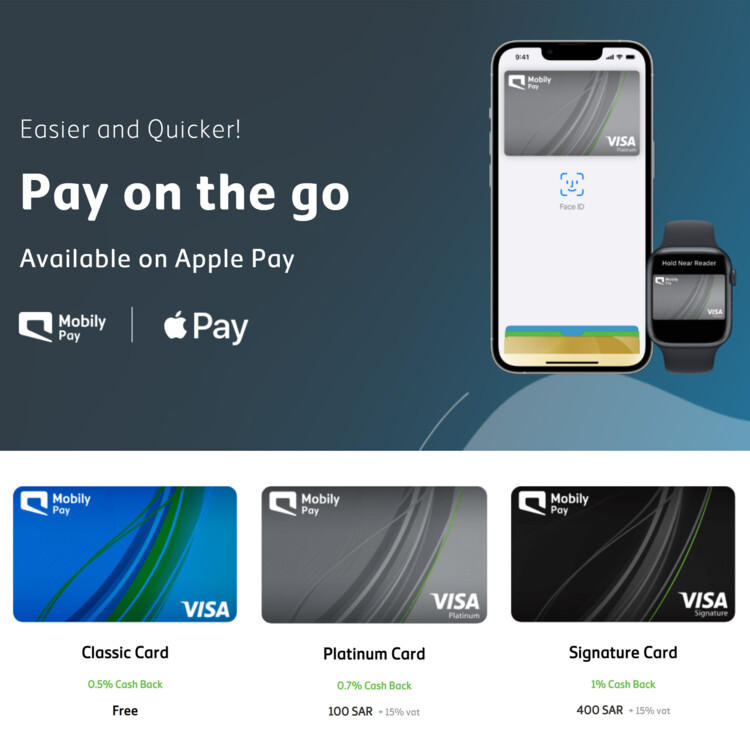

One of the most significant developments in embracing an open approach for mobile money is partnership with card schemes like Visa and Mastercard. Mobile money providers have partnered with these companies’ schemes to issue co-branded physical and digital companion cards. Companion cards can be used by mobile money users to make physical point-of-sale or online payments to Visa and Mastercard accepting merchants globally, despite these merchants not being registered in the mobile money system. Consumers can also withdraw money at ATMs using companion cards. For example, Mobily Pay users in Saudi Arabia can instantly request and get a digital Mobily Pay Visa card in the Mobily Pay mobile app. Mobily Pay users can use the digital Visa card to make online payments or make tap and go payments at near-field communication (NFC) point-of-sales terminals. The Mobily Pay Visa card can also be added to Apple Pay, making third-party wallet transactions possible. Companion cards extend mobile money acceptance beyond registered merchants, making them part of open and global services.

Image source: https://mobilypay.sa/

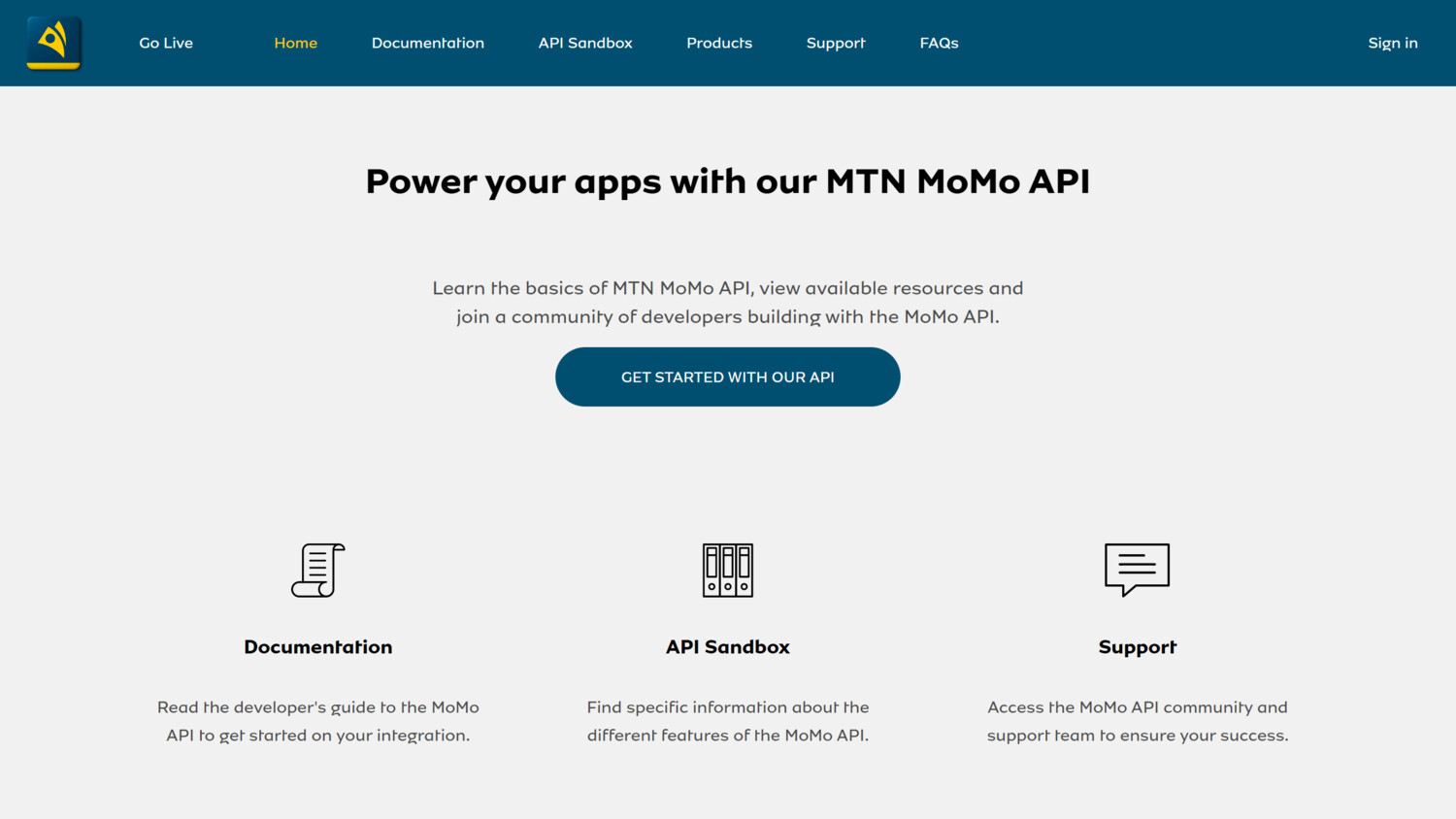

The biggest move toward the open financial ecosystem is the introduction of mobile money open application programing interface (APIs). APIs define how two types of software communicate with each other using requests and responses. Conventional banks and financial institutions lack an API infrastructure, and mobile money providers only expose their APIs to selected third parties. However, in the last few years, mobile money providers like MTN MoMo and Orange Money have embraced an open approach and launched the Open API platform and developer portal, to provide all third-party developers free access to their mobile money proprietary software platform. These mobile money APIs can be used by all third parties from big enterprises and e-commerce companies to small merchant and start-ups to create innovative financial services and applications. Developers get access to the API Sandbox that provides a testing environment similar to the live production environment. It helps developers to thoroughly test their application by stimulating a response from the APIs it relies on, reducing the risk while deploying the application in a live environment. This has resulted in a huge success for Open APIs. MTN had 17,948 developers experimenting with MoMo Open APIs in the platform’s Sandbox and 948 third party partners live in production by 2021 (Source: MTN 2021 Annual Report). The APIs are being used to create novel financial and payment services such as pay-as-you-go solar energy, real-time international remittances, pay-as-you-learn low-cost school networks, ride-hailing service payments, AgriTech payments, HealthTech payments, mobile savings, digitalization of credit cooperatives, mobile-enabled insurance services, crowdfunding, bulk disbursements and more.

Image Source: https://momodeveloper.mtn.com/

5. Architecture axis evolution: from monolithic to micro-services cloud-native architecture

Most mobile money services, which were introduced a decade ago, started with monolithic architecture. In monolithic architecture the entire mobile money application is designed, developed and deployed as a single monolithic unit. However, the challenge with monolithic architecture is that it is difficult to seamlessly support the rapid growth of mobile money customers, transactions, use cases and integrations. The larger the application, the more difficult it becomes to deploy new features and changes. Hence, most mobile money services are shifting to micro-services architecture. Here, the mobile money application is broken into smaller services which are loosely coupled. Each smaller service, which is called a micro-service, performs a specific task.

Micro-services architecture brings a modular approach to development, where updates can be performed on one micro-service independent of the rest of the application. This supports agility in application development and faster changes and version roll outs. Micro-services architecture also helps with easier fault isolation and correction. In case of a fault in one micro-service the entire application will not shut down. When the error is fixed, it has to be deployed for the impacted micro-service, rather than for the entire application.

Benefits of micro-service architecture are augmented by a cloud native approach. A micro-services architecture with cloud native capabilities improves scalability, as each micro-service can be independently scaled, depending on load. Hence, the number of instances of a micro-service can be increased during high load and decreased during low load, providing efficient load regulation, and optimizing cost. The cloud based approach is particularly beneficial for mobile money providers serving multiple countries from a centralized application. These mobile money providers can adopt a multi-tenant cloud approach sharing the computing resources across tenants (countries), enabling economies of scale.

Another focus area is DevOps, where Continuous Integration and Continuous Delivery (CI/CD) is bringing positive changes. CI/CD introduces automation in various stages of application development, such as code integration, testing, delivery, and deployment. The changes made by the developers in the code are automatically tested and released for delivery and deployment, accelerating the development and deployment process.

6. Security axis evolution: from basic to advanced security

During their early days, mobile money services were introduced with basic security features—pin or password-based access (single factor authentication), regulator prescribed transaction limits, compliance with basic KYC and anti-money laundering (AML) rules, standard data encryption and more. However, with the scaling of mobile money services, the threat of security breaches and sophistication of fraud has increased multifold. Hence mobile money providers have stepped up the fight again fraud and moved to advanced security measures.

Mobile money providers are now using multi-factor and strong customer authentication. They can use either one or a combination of factors such as a pin or password (something only the user knows), an OTP (something only the use possesses) or biometrics (something the user is) for authenticating the user. Device binding where device credentials are linked to user accounts and mobile apps adds another security layer in multi-factor authentication. Different access channels like mobile apps, USSD, and the web can have different combinations of multi-factor authentication.

Sophisticated rule engines, AI and data analytics are being used to identify anomalies in consumers’ transaction trends and raise alerts and send notifications in real time to curb frauds. Advanced fraud management systems do transaction velocity checks and detect transaction spikes, high value transactions, cyclic transactions, duplicate transactions, and other anomalous transaction behavior, and send out alert notifications to concerned parties to warn about frauds. Advanced fraud management systems can also map and analyze the connections and networks of fraudulent users. When barred or fraudulent users are identified, the connections with whom they transact are also identified and mapped. The transactions between the fraudulent users and connections are analyzed and suspicious connection accounts are also blocked from carrying out transactions and prevent potential frauds.

Location tracking of consumers’ mobile devices has also become an important tool in fraud prevention. For example, while depositing or withdrawing cash at an agent, if a consumer’s location is tracked through a mobile phone and is found to not be in close proximity with the agent’s location, then the transaction can be rejected as a fraudulent transaction.

Biometrics is increasingly being used in various consumer activities. The most common one is use of fingerprint or face ID while logging into a mobile money app or authenticating a transaction on a mobile phone. Biometrics is also employed in mobile money registration and KYC processes to authenticate users. It is also used to validate users when they withdraw cash at the agents, especially in a situation where financial aid is disbursed through agents to refugees or underprivileged people impacted by poverty and natural calamities. Mobile money agents, in areas such as refugee settlements or recipient villages, are provided biometric devices to capture the fingerprint or iris scan of users and identify the legitimate recipients. GSMA B4LL (Biometrics for all) initiative is working with Easypaisa Pakistan to leverage voice biometrics and provide a voice enabled IVR call center experience for Easypaisa users.

Conclusion

As the world advances further into the digital payments age, it becomes critical for mobile money providers to progress on all the six axes discussed above, to create value for their customers and eventually their own business in the future. This also means mobile money providers need to choose a futuristic mobile money platform partner that can help them to evolve their mobile money services across all the six axes.

Ericsson Wallet Platform helps mobile money providers to grow simultaneously on all six axes—access channel, services, experience, ecosystem, architecture, and security. Ericsson Wallet Platform delivers a consistent experience across channels ranging from USSD to apps and the web and helps mobile money services to progress on the path to become financial super apps. It is enabling mobile money providers to elevate consumers from financial inclusion to financial wellness by facilitating advanced services like savings, loans, overdraft, digital cards, buying items on credit, insurance and investment. Ericsson Wallet Platform is encouraging the use of rule engines, AI and ML to deliver more personalized and enhanced financial service experience to consumers and empower them to have better control over their money. The platform is also promoting an open ecosystem providing a wide range of APIs enabling mobile money providers to rapidly integrate with third parties to build an interconnected ecosystem with partners and launch innovative mobile financial services together. Ericsson Wallet Platform is also helping mobile money providers to adopt micro-services cloud native architecture aimed at bringing seamless scalability, faster service rollouts and operational efficiency. It is also providing advanced fraud management capabilities to strengthen the security of mobile money services to fight the growing threat of frauds and security breaches. All in all, Ericsson Wallet Platform is helping mobile money providers to excel in the present and prepare for future growth. Learn more about the platform here.

Missed part 1 of this blog series? Read from here

Related content

Read about Ericsson Wallet Platform

Read our Ericsson Perspectives article: The future of money: How digital ecosystems are changing our understanding of value and trust

Read the report on mobile money in Sub-Saharan Africa Mobile financial services on the rise (pdf)

Learn more about CI/CD and how it can unleash faster software delivery, improved quality and continuous innovation across your network operations.