5G and opportunities for compelling new services

- English

- 繁體中文

Service providers benefit from service bundling as well as connectivity revenue from the most popular applications.

- Many service providers are moving towards content aggregation, removing most of the risks associated with traditional bundling.

- Connectivity still represents the core value for service providers.

- Service-based connectivity packages are a step towards value-based pricing.

Mobile networks have evolved and now deliver capabilities beyond what most individual services require. However, the low latency and vastly improved throughput in 5G networks are expected to lead to new, exciting services being developed in the future. This is especially the case in moving imagery, and can already be seen in gaming and VR or AR.

Low latency allows for moving some or all of compute or rendering capabilities into the cloud, which in turn allows for cheaper, lighter devices and longer battery life. This is especially evident when looking at the XR device ecosystem, which will potentially benefit through earlier availability of such devices.

Consumers place new services high on their list of expectations from 5G, and also say they are willing to pay for these services.1 Many of the highly attractive services come with a monthly fee, like music or video streaming services and cloud gaming or some of the AR and VR applications already available. The question is, in what ways can service providers benefit from such services?

Services enrich the business

It is common to add “sweeteners” or “value items“ to the service offerings as a way to differentiate and create additional value. Service providers may add roaming data, virus protection or device insurance to the plan, but the more popular items used when bundling with smartphone subscriptions today are third-party video or music streaming services.

Of all service providers offering 5G, around 45 percent have been bundling third-party services. Earlier, they would sign exclusive agreements with a streaming provider to differentiate and attract more subscribers than their competitors. Today, the streaming market is mature and such agreements are commonplace, so this is seldom an option.

Traditional bundling is now a way to attract users to specific packages, typically towards premium subscriptions. The data bucket model has connectivity itself as a major part of value differentiation, but for the unlimited model, the value items have that role entirely. Interviews with service providers2 reveal that the most effective way of selling bundles is through campaigns and short-term offers, where content services are offered free for a few months. Once that time has passed, consumers typically choose to keep services which they value. In the past year, the impact of global inflation has led to several service providers discontinuing traditional hard bundles completely. Interviews with service providers have shown that hard bundles have become associated with issues such as price changes and tough contract terms from content owners, deterring some service providers from introducing bundles or leading to a decision to discontinue them.

Some also mentioned that the attraction of individual services may change over time. For example, a new series from a video streaming service provider may become immensely popular and as a result that streaming platform gets a sudden rise in interest. Later, when all the episodes have been aired, people may want to move to another service.

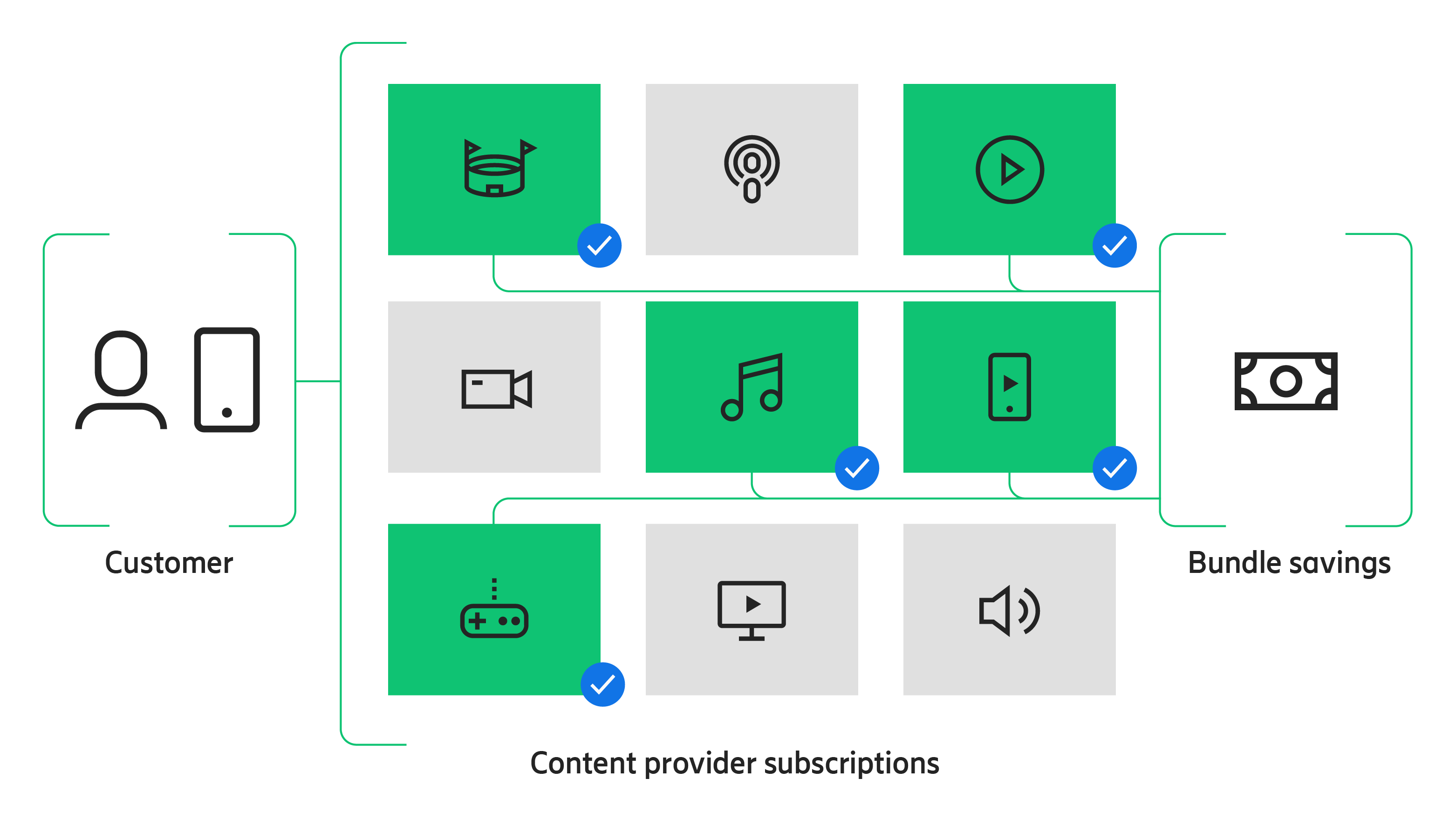

Many service providers are now starting to act as content aggregators, whereby they offer a much larger variety of services to their consumers. These services are offered as flexible bundles added to a plan without being tied to the base price of that plan. This structure also allows for selling across all customer segments, regardless of tiers. It may even be offered to all consumers in the market as an “over the top” service. Besides the most commonly offered third-party streaming services, there may be magazine subscriptions, news services or training programs. The most proactive content aggregators offer the ability to add and remove service subscriptions on a monthly basis, without the bundle affecting or being affected by the base plan.

There are several benefits with this model:

- Consumers have full flexibility of choice from most or all services in a single place and on one bill.

- Service providers receive a share of the monthly fee from each of the included services.

- Consumers with many services will be less likely to churn.

- Services drive traffic and many subscribers may need to upgrade their base subscription to higher data tiers at some point.

- Streamlining processes using APIs can reduce cost and effort while speeding up the onboarding task significantly.

- The risks associated with hard bundles are more or less eliminated as the price of the content service is not linked to the price of the connection.

Figure 6: Service providers‘ new role as content aggregator

Service and connectivity hand in hand

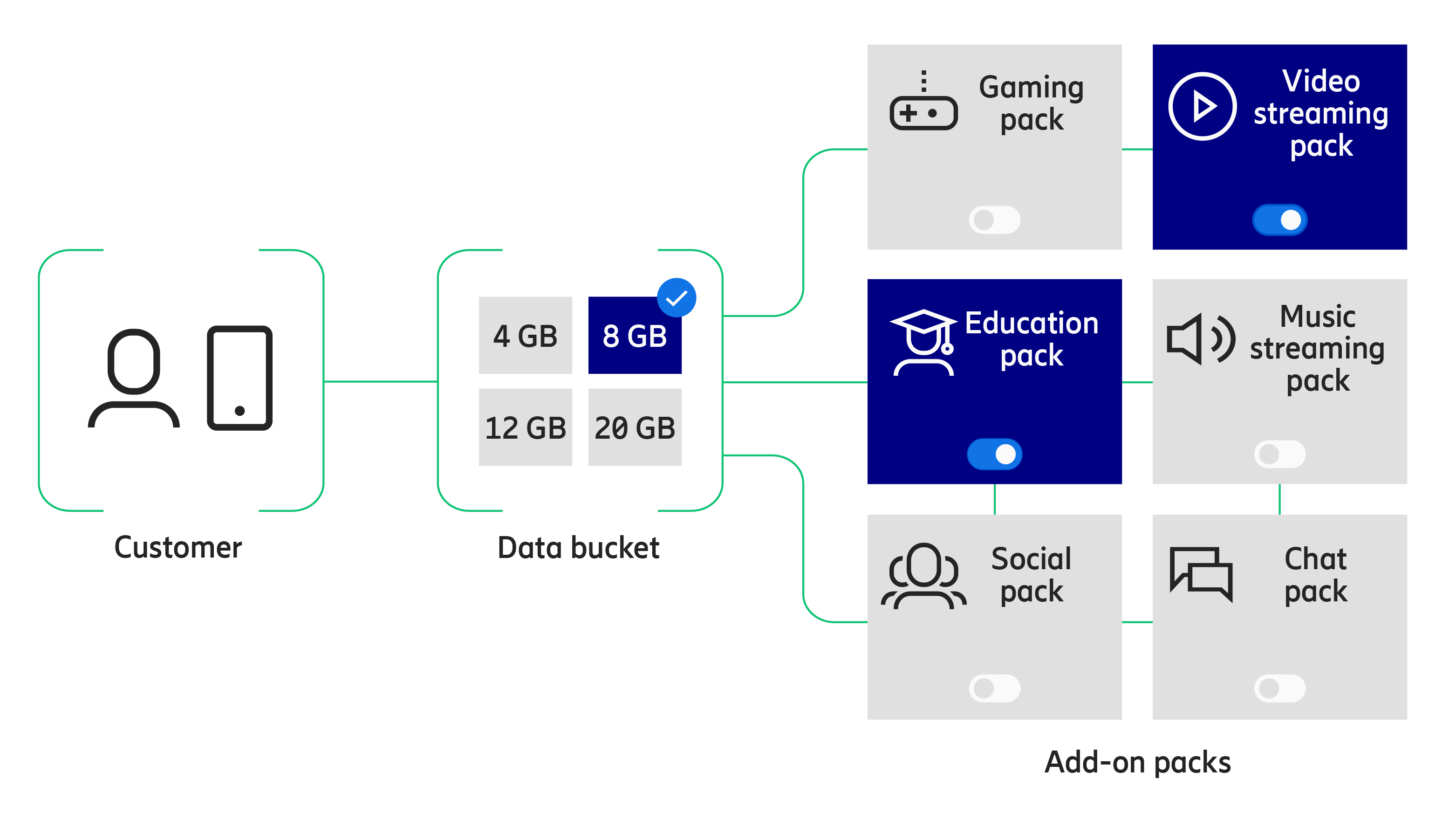

The use of service-based connectivity offerings has increased recently and, as the name suggests, they provide connectivity to be used only for a specific type of service, such as video streaming.

Service providers often call this type of connectivity “passes” or “packs” and they are usually named by the service they are intended for, like “video pass” or “music pack”. These passes are added on top of the base plan and the most common variants provide either gigabytes to be used only for a specific purpose, for example video streaming, or for allowing completely unlimited video streaming, in both cases without consuming from the base bucket. There are also those which sell “buckets of hours” which may be easier for consumers to relate to as it correlates with their usage patterns. The segmenting factor for such packages becomes the monthly number of hours of video, music or perhaps cloud gaming.

Nearly 40 percent of service providers have some type of service-based connectivity targeting traffic-intense video or music streaming services. Interviews reveal that service providers are very happy with this type of packaging, and there is high interest in using them for new and demanding services like cloud gaming.

The basic reasoning behind service-based connectivity is that it:

- connects usage and revenue, as the packs can be designed with price tiers in relation to specific factors such as time spent or data used

- provides an alternative to unlimited data with the ability to use popular services as much as consumers need, without worrying about running out of base subscription data or incurring high costs

- allows for more of a value-based pricing principle within each individual service category

- creates a connectivity-related revenue stream for services that the service provider does not even need to own

- allows for a more granular segmentation of the market, which in turn allows for attractive pricing compared to, for example, unlimited.

Customer awareness is key

Some new services like cloud gaming and VR/AR may generate many times more traffic than streaming video. Revenue will come from these services through retail partnerships, similar to what exists with video and music streaming providers. However, the load on the network from these services is higher and often there are costs involved from investments in platforms and servers. A business model such as service-based connectivity, which also allows for monetization of the connectivity for these services may, therefore, prove to be crucial.

There is however a risk that consumers may be unaware that such options exist. This applies to both aggregation bundles and service-based connectivity passes. They are not necessarily part of the standard subscription and therefore need to be selected and added by the subscriber themselves. However, as mentioned already, promotions and campaigns are effective ways of raising consumer awareness. Another way to resolve this, starting to be used by some service providers, is to integrate this type of packaging into the customer journey. This is done by placing it into the process of buying the basic SIM card subscription. This starts with the selection of a data plan or bucket, ending up at a menu where the customer gets to select their entertainment services and/or the connectivity passes to go along with these. All is added up to the final price, taking into account any potential discounts that may be accrued.

Connectivity still represents the core value

Without connectivity, it would be impossible to enjoy all the services and apps used on an almost daily basis. Service providers are in the fortunate position of being able to aggregate content and offer a wide variety of subscription services in a digital marketplace. This marketplace may even become a valuable asset in itself, providing visibility for content providers while being simple, flexible and easy to use for consumers.

For the content providers, it is undoubtedly beneficial to be part of these ecosystems, which is why they are willing to share revenue with service providers. Meanwhile, for the service provider, it is important to also have models, like service-based connectivity, which allow for monetization of the core of their business, namely connectivity. Although it may be some time until networks are fully upgraded to 5G SA, with slicing, as networks evolve, there is potential for service providers to take even further steps towards more flexible and advanced packaging. This might be more closely mapped towards the value of both the services themselves and the experience provided by the connectivity they are relying upon.

Figure 7: Integrating service-based connectivity into the customer journey

1 Ericsson Consumer & IndustryLab, 5G: The next wave.

2 Interviews with 10 service providers from November 2022 to January 2023.