Is it still worth to invest in 5G in a flat revenue scenario?

- English

- Français

5G Strategy and Innovation Director

5G Network Evolution Driver

Commercial Director

5G Fixed Wireless Access driver

5G Strategy and Innovation Director

5G Network Evolution Driver

Commercial Director

5G Fixed Wireless Access driver

5G Strategy and Innovation Director

5G Network Evolution Driver

Commercial Director

5G Fixed Wireless Access driver

5G enables new monetization levers

5G is already enabling a set of innovative monetization levers for CSPs across multiple domains, such as:

- unlocking revenues’ potential in the underpenetrated Enterprise segment through private networks, mission critical networks and differentiated connectivity over the macro networks

- increasing ARPU in the consumer segment through innovative performance differentiated offering, speed-tier pricing and bundling of advanced services such as cloud gaming and XR/VR content

- addressing underserved fixed broadband market areas through FWA connections

As the net effect of such monetization levers depends on the specific market maturity, operator positioning, competitive market dynamics, and digital ecosystem readiness, all CSPs are carving their own strategy to translate the monetization levers into top-line growth.

The pressure on the GB

At the same time, we witness continued and sustained mobile data growth over mobile networks, with expected growth rates for most world regions in the range of 20% to 30% for the upcoming 5 years (source Ericsson Mobility Report June 2022).

Given the highly competitive market dynamics, this growth in mobile data volumes does not necessarily translate into ARPU growth. In fact, we witness strong pressure on total mobile service revenues per GB. According to Tefficient Market Analysis (Tefficient - Industry analysis #1 2022 - Mobile data – full year 2021), the total mobile service revenues per GB decreased from 2020 to 2021, ranging from -9% to -35% for 28 tracked countries.

Independently from top-line upsides, the combination of these trends calls for the most efficient way to carry the expected growth of mobile data volumes.

Investing in 5G in a flat revenue scenario

In light of this context, we put ourselves into a theoretical scenario whereby we assume no short-term top-line growth from introducing new services.

We then developed an analysis to answer a basic question: in the absence of incremental revenues from innovation in pricing, services, or markets, is it still worth investing in 5G?

Our analysis compares two possible scenarios, one where an operator continues to expand its LTE network; another where he moves immediately to 5G SA with mid-band 5G spectrum to build the needed mobile data capacity.

Total Cost of Ownership (TCO) is calculated considering initial investments (CAPEX) and ongoing costs (OPEX) for the incremental Radio, Core, and IT components.

The starting point

In order to answer such a question, we modeled a representative base case that many mobile telecom operators may be facing. We took an urban cluster of 1000 LTE sites with deployed capacity in the lower and higher LTE bands and assumed a current capacity roll-out of 60% in both bands and a 90% utilization of the current deployed capacity. Finally, we considered the Mobile Broadband service with an expected 5-years data growth rate of 23%, representative of Western Europe.

The scenarios analyzed

Based on this starting point we developed two alternative scenarios to cater to mobile data traffic growth:

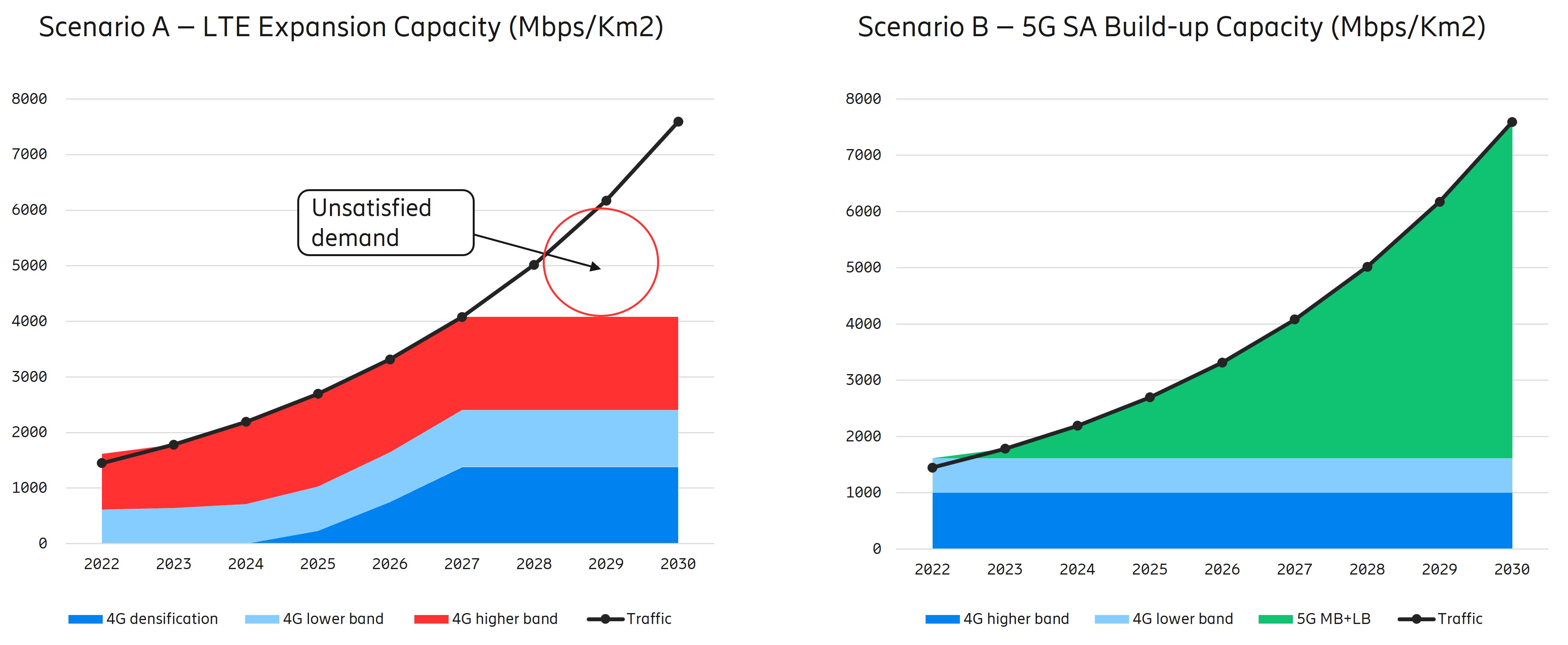

- Scenario 1 - LTE Expansion, whereby the emerging mobile data traffic needs will be satisfied by deploying the remaining LTE capacity on lower and higher bands, followed by site densification as the available capacity fills up

- Scenario 2 - 5G SA Build-up, whereby no LTE expansion will take place and all the new capacity will be deployed on 5G mid-band and low-band, and the full 5G Standalone (SA) architecture will be deployed

Ability to cope with expected mobile data traffic growth

Taking the year 2022 as a base in the LTE expansion scenario, after saturation of the existing LTE capacity, new lower and higher band capacity will be added on existing sites. As LTE high-band is fully deployed, densification will be needed. Densification will reach a physiological limit in 2027, after which extra traffic demand cannot be satisfied.

In the 5G case, after the saturation of existing LTE capacity, increased traffic demands will be served by the deployment of 5G MB TDD and LB capacity on the existing LTE grid. The 5G capacity expansion can satisfy traffic demand up to 2030 without the need to densify. The subsequent TCO analysis runs with a horizon of 5 years (ending 2027), not to project unrealistic LTE densification.

TCO Network Model

In our TCO Network Model, we’ve considered the needed network CAPEX and OPEX for a mobile operator to build incremental capacity.

The following components have been taken into consideration: Radio Access Network, Sites, Core Network, and Transport Network.

Operators can achieve 54% lower TCO

By implementing extra capacity directly on 5G SA, operators can achieve 54% lower TCO. The result of our modeling clearly shows that 5G SA with TDD mid-band build-up is consistently more cost-efficient than 4G expansion. The cumulated TCO advantage of 5G vs. 4G to build the incremental capacity is 54% over the 5 years.

5G cost advantage has been growing over the years from Y2. The advantage becomes greater as 4G densification occurs.

Cumulated Cash Out (CAPEX+OPEX) - MEUR

Drilling down on the CAPEX and OPEX TCO components over the 5-year period, our findings show:

- a 49% CAPEX advantage of 5G SA vs. LTE. In the case of LTE expansion, the CAPEX required to match estimated traffic growth is dominated by RAN and Site construction driven by LTE densification

- a 65% OPEX advantage of 5G SA vs. LTE. Key drivers of 5G cost advantage are reduced sites OPEX and energy costs

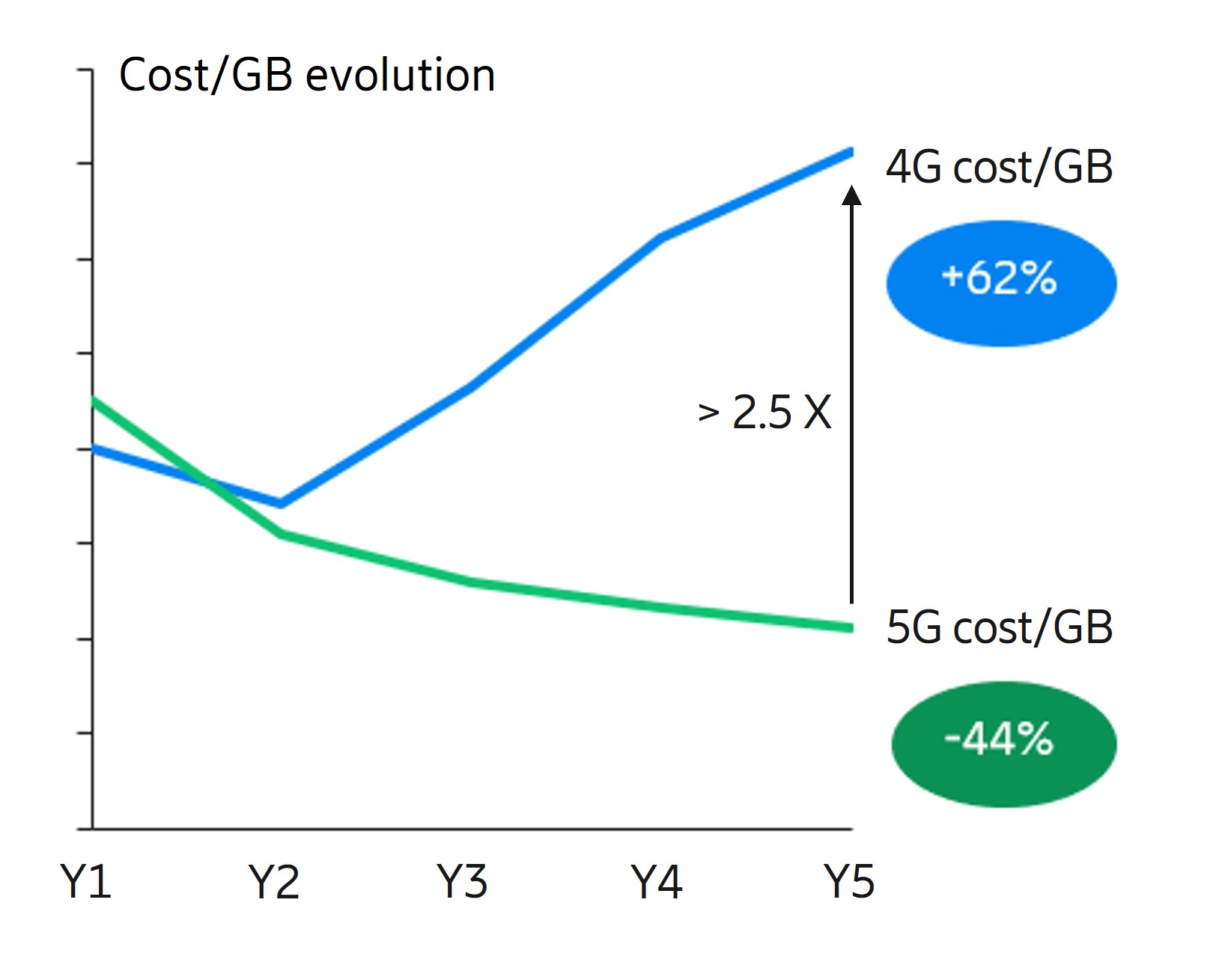

5G as the only viable option to decrease cost/GB

The strong 5G advantage translates into a lower cost/GB as traffic grows:

- for LTE Expansion the cost/GB shows an increase over the years (+62% in 5 years)

- in the 5G SA case the cost/GB decreases (-44% in 5 years)

On Y5 cost/GB on 4G is >2.5X times greater than the corresponding in 5G, making 5G the only viable way forward.

5G wins the energy efficiency race

Given the actual turbulences in the global energy markets, we had a closer look at the respective energy consumption of the two analyzed scenarios.

The results of the analysis show that for the considered cluster, 4G Expansion requires 4X times more energy compared to the 5G scenario. This is a consequence of 5G being a more energy efficient technology compared to LTE thanks to “3GPP NR lean design” with system information overhead reduction, of the higher spectral efficiency of 5G vs. 4G and of the lower energy footprint of the new 5G Ericsson Radio portfolio.

Cumulated Energy consumption over 5yrs timeframe, MWh

The lower energy consumption directly reflects in the energy bill.

Given the current volatility of energy prices, we have run a sensitivity analysis (taking a reference price of 0,15 Eur/KWh) on the impact of the potential energy price surge on the OPEX component.

In the 4G case, energy costs constitute a larger share of total OPEX with respect to 5G, and a surge in energy prices would mean a higher overall impact.

Energy costs as % of total OPEX

A surge in energy costs would severely impact 4G OPEX, while the effect on 5G SA OPEX would be moderate.

Cumulated 5yrs OPEX - M€

So, we could say that going 5G will implicitly give operators insurance to edge energy price volatility.

Conclusions

The result of the analysis clearly shows that for dealing with the forecasted mobile data growth, an operator’s more convenient TCO option is to build the incremental network capacity directly on 5G SA.

5G SA will also enable new service revenues, such as AR/VR, Slicing, or Exposure, thus further improving the overall operator business case.

A summary of 5G SA advantages is shown in the table below.

LTE expansion scenario |

5G build up scenario |

|

| Ability to satisfy mobile data growth | Unable to fulfill expected demand beyond Y5 | Full support |

| Execution Complexity | Requires antennas densification that might be complex in an urban scenario | 5G Radio and Core implementation |

| 5Y TCO (CAPEX + OPEX) | More expensive | -54% TCO over LTE Expansion scenario

|

| Cost/GB | +62% over 5 years | -44% over 5 years |

| Energy Consumption | More energy hungry, more exposed to energy price surge | -76% energy consumption with respect to LTE scenario |

| Capture revenues from new segment/services | Moderate. Support for speed, but lack capabilities for latency, slicing, AR/VR | Full support. Enable industrial use cases, slicing and API Exposure for Consumers and Enterprises |